The Coming Economic Collapse

The Coming Economic Collapse

Part IV: The fraudulence of central bankers and the limits of their power (Free)

Issues discussed:

The (short) history of financial market bailouts by central banks.

Central banks have resorted to some serious ‘accounting-wizardry’ to hide their massive losses.

The ability of the central banks to respond to the approaching economic collapse may become seriously hindered.

In December 2017, we noted in the Q-Review of GnS Economics (Approaching Perfect Storm) that:

If the central banks and China really go through with their plans, noting that China can also just run out of options, 2018 is likely to be the year, when the first signals of the crisis will appear. These include serious market turbulence, bank failures and possible panicky responses from the central authorities. In 2019, the crisis would get to the full swing when the last efforts of the central authorities to uphold the global asset bubble would become exhausted.

2018 actually was the year, when the first signs of the crisis appeared. Market volatility started to grow in October, reaching its peak in and around New Years, leading to the infamous ‘pivot’ by the Fed on January 4, 2019. In 2019, the crisis got into full swing with the near-collapse of the repo-market of the U.S. in mid-September. After that, the Fed re-started its QE-program, dubbed as “Not-QE” as The Federal Reserve bought short-maturity Treasury Bills (instead of Notes it bought in “original-QE”). This was of course nothing but trickery regarding the name of the program. It did the same as the “original QE”. That is, it increased liquidity in the hands of investors by buying what they were holding with newly created reserves (and thus money) through the banking sector (see my explanations, e.g. from here and here).

The bailout operations by central banks and governments have created a new layer of uncertainty in economic forecasting. What worries me the most is what if they some day decide that they will not bailout the financial system anymore, or they are unable to do so?

I conclude this piece by noting that:

So, we have to acknowledge that, this time around, central bankers may not be all-powerful. This implies that when the collapse truly commences, there’s no certainty that the bailouts come or if they come (at first), they can be limited with likely devastating consequences.

Let me explain.

The short history of bailouts

While Federal Reserve took (some) action after the Great Crash of 1929, the market bailout policy of the Fed truly began during the tenure of Chair Alan Greenspan.

On Oct. 19, 1987, on “Black Monday”, the U.S. stock markets collapsed. The Dow Jones Industrial Average fell by (around) 20 percent, its largest percent-wise daily fall ever. Before markets opened the next day, Alan Greenspan issued a statement in which he pledged to “serve as a source of liquidity to support the economic and financial systems.” The Fed also dropped its fund rate to 7 percent from 7.5, and injected liquid reserves to markets. The crash was halted, and the term ‘Greenspan put’ was born. It described a policy doctrine, where the Fed allowed the markets to rise freely and then enacted a ‘bailout’ of the markets after they collapsed. Greenspan used it several times during his tenure, which ended with his retirement on 31 January, 2006.

To describe the commonality of central bank bailouts since the GFC (Great Financial Crisis), I will re-publish a list of financial market bailouts by central banks from my May 2022 Epoch Times article:

In late November 2008, the Fed announced it would start buying the debt of government sponsored enterprises in the secondary markets in programs called quantitative easing, or QE. In March 2009, the Fed extended the program to include U.S. Treasuries.

In October 2010, the Bank of Japan started to buy Exchange Traded Funds linked to the Japanese stock market. It became customary that the bank would begin buying whenever the Topix stock market index fell more than 0.2 percentage points by midday.

In August 2012, the European Central Bank enacted the Outright Monetary Transactions (OMT) program to halt the rise in sovereign bond yields in the Eurozone. In 2015, in an effort to devalue the Swiss Franc, the Swiss National Bank started to “invest” in foreign assets, including U.S. equities. In many cases, such purchases by the SNB coincided with increased market turbulence/risk, as during the first actual post-Global Financial Crisis rate hike cycle of the Fed in 2016/2017.

In 2017 central banks across the globe pushed over $2 trillion worth of artificial central bank liquidity into the global markets in a ‘Liquidity Supernova’. In December 2018, the People’s Bank of China started to support the domestic banking sector by injecting hundreds of U.S. billions worth of liquidity into the system.

On Jan. 4, 2019, due to a threat of an outright collapse of the stock and credit markets, Fed Chairman Jerome Powell ‘pivoted’ from his previous statements of several interest rate rises and automated balance sheet run-off in 2019. Between January and March 2019, the Federal Reserve made a complete U-turn from its earlier stance of several interest rate rises in 2019 to possible cuts and ending the balance sheet normalization program prematurely.

On Sept. 17, 2019, the repo markets clogged up and the Fed started its repo operations on the following day. On Oct. 16, 2019, the Fed started to buy U.S. Treasury bills at the rate of $60 billion per month.

In March 2020, the coronavirus outbreak was freaking out the markets, and on March 16, 2020, they crashed. The volatility index reached 82.69, the highest on record. The Dow Jones Industrial Average plunged by 2997 points, or 12.9 percent—the worst point drop on record.

On the 16th, the New York Fed announced that it will add $500 billion in the over-night loans to repo-market. On the 17th, the Fed announced that it would use $1 trillion to mob up corporate paper from issuers. On the 18th, the European Central Bank announced that it would buy 750 billion euros worth of bonds and securities. On the 19th, the Fed announced that it would create lending facility to money market mutual funds. On March 25, 2020, interest rates of short-term corporate debt surged to 2.43 percent above the federal-funds rate, the over-night lending rate of the Fed, which led the central bank to issue a program targeted at the corporate markets.

So, the history of market bailouts by central banks is long and it has turned ever more pervasive during the past five years. The limitations for this “printing” are likely to come from the political side.

The likely response of the Federal Reserve

In December 2017, when discussing the uncertain path ahead, we noted that:

Growth outcomes are heavily dependent on central authorities unprecedented actions and their ability to keep the global asset bubble inflated.

So, I have been asking myself for quite some time, what will central banks do when the recession and collapse come. Now I find myself asking, can they enact further bailouts, and if so, on what scope?

In the U.S., if (when) interest rates are properly lowered, or even pushed back to ZIRP (zero-interest-rate policy), the U.S. federal government can, most likely, continue to rack up their massive debt pile for a bit longer without any serious problems (like a no-demand auction cancellations for Treasuries). Yet, if the financial crash is a proper one, it may even create problems for the Treasury to keep issuing large quantities of debt-paper, because investors can become wary of a possible U.S. default. Here, naturally, is where the Fed steps in.

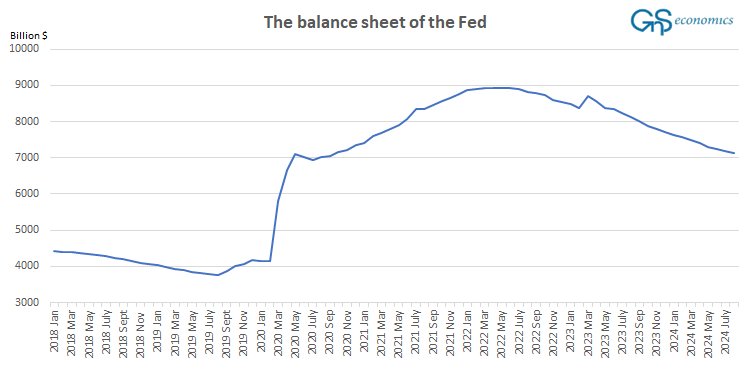

During the spring of 2020, we saw a massive bailout operation of the U.S. financial markets, like noted above. The Federal Reserve effectively backstopped the U.S. Treasury markets, intervened in corporate commercial-paper and municipal bond markets and short-term money-markets. The effect of this on the balance sheet of the Fed was nothing short of cataclysmic. In just three months, the balance sheet ballooned by €3000 billion, while more than doubling before reaching its peak (for now).

This figure below shows the downdrafts of late 2018 and Spring 2020. The 2018/2019 crash ended to the ‘pivot’ of the Federal Reserve, and 2020 crash to an bailout of the financial markets by the Fed, like explained above.

It is very likely that the Fed would continue this policy line also in the approaching collapse. That is, when the panic starts, the Federal Reserve will, most likely, try to give support to every corner of the financial markets, where needed. Other central banks would very likely follow. However, is not so clear cut this time around, whether they are able to issue an extended bailout to the financial markets and the economy. Their options may become gravely limited by inflation and politics.

Losses of a central bank

A central bank earns income in the form of interest from its holdings of securities. If the liabilities contain just required central bank reserves and currency, the central bank has “zero-cost” of financing. If the liabilities include any excess reserves and foreign or domestic liabilities, the central bank pays an interest. In general, the value of foreign and domestic assets have a significant role in a central bank’s income stream. Losses to a central bank tend to arise from interest obligations, subsidy payments, multiple exchange-rate practices, “guarantee” schemes and unfavorable changes in net asset valuations. The QE programs made central banks especially vulnerable to the last of these.

Miguel Castro and Samuel Jordan-Wood summarized the income stream of the Fed as:

We can think of the Fed’s net income as being, roughly, equal to the product of the net interest rate spread (the difference between the interest rate earned on assets and the interest rate paid on liabilities) and the size of the Fed’s balance sheet. Monetary policy tightening can reduce net income by reducing each of these components individually.

When a central bank accrues a loss beyond its stream of net interest rate income, that is gross interest income minus expenses, and seigniorage, it starts to eat through the capital of the central bank. Essentially, a central bank follows normal accounting practice. However, because the central bank has control over the monetary base (currency + reserves), it can create demand for its liabilities (currency) by buying government securities and earn seigniorage. This is the crucial difference between a central bank and a commercial bank. The central bank can claim to be solvent due to the future income stream from seigniorage, even with negative net worth, which a commercial bank cannot.

But, covering a large loss from seigniorage will require a large growth in its monetary base, which tends to be highly inflationary (I’ll explain the basic mechanism of this below). So, while a central bank can, technically and theoretically, cover all conceivable losses, this can only be accomplished through massive increase in the monetary base, which tends to lead to very high inflation and, in the worst case, to the destruction of the monetary system through hyperinflation. The other option is that the government covers the losses of the central bank.

Some central banks have managed to operate relatively effectively also with negative net worth, which would mean insolvency of any other financial institution or a firm. However, this is considered to be a highly risky maneuver which can, and often has led the central bank to lose control (trust) of the financial markets. This is why every modern central bank tends to have rules in place for their recapitalization. Now, they have drifted into some very questionable accounting practices.

Accounting wizardry

What comes to Federal Reserve, it has accrued massive “paper” losses. How does it handle these?

Like explained above, and now argued by the Fed, in a technical sense these do not matter, because the Fed can assume to accrue seigniorage revenue ad infinitum. Thus, it claims to be solvent. The European Central Bank has taken a similar policy stance, labelling the losses as deferred assets, which “will be carried forward on the ECB’s balance sheet to be offset against future profits.” This means that they have marked these losses as positive assets in their balance sheets and income statements. How can this be?

William Buiter, one of the great living scholars of central banking, noted in March that:

Following this logic, why not allow a shareholder-owned private company to include losses that would take the firm’s capital below some threshold level as a deferred asset (or a negative liability) on its balance sheet? After all, the privately owned company is obliged to remit excess earnings to its shareholders after accounting for operating costs, debt service, and any amount necessary to maintain a surplus. The corporate deferred asset would be the amount of future net earnings the company would need to realize before payment of dividends to its shareholders can resume. Obviously, this would be economic and financial nonsense.

The reason both central banks have entered into this “accounting-wizardry” is, 1) because they can due to seigniorage, and 2) if they would mark them as losses, they would eat through their capital forcing banks to operate with a (deep) negative equity. In history, this has had the tendency to create notable uncertainty in the financial markets, as investors have started to suspect what is really driving the decisions of a central bank: the needs of the economy or the need for the bank to cover its losses. Serious questions would also, at some point, be raised by authorities. Covering such a heavy losses from the seriously over-stretched government budgets would lead to a political outroar, with an extreme backlash. This is why central banks are trying mask their devastating losses as “assets” from future income. From an accounting perspective, this is nothing short from fraudulent. Yet, authorities and economists will allow this nonsense to fly, because they are afraid of criticizing their cherished institutions despite of them becoming utterly corrupted. Many probably also fear what would come if central banks would lose their grip on the economy and free markets would return. The corruption of my profession (macroeconomics) cannot get much deeper.

Alas, with the consent of politicians and economists alike, central banks have invented a ‘perpetual motion money-machine’, where they can print any amount of money, buy any amount of assets and declare all losses accrued on them as “assets”. This is utter nonsense.

For us, the question now becomes, in the case of another financial collapse, for how long can the central banks carry the financial markets and system?

Hyperinflation as the backstop for monetary manipulation?

The answer to the question posed above is: as long as politicians allow or inflation forces central banks to stop. Central bankers have set their selves a trap.

The QE program is essentially a credit line of the central bank. Using it, the central bank buys an asset, usually a government or corporate bond, from investors through one of the so called Primary Dealer banks.1 It thus creates money in the process of buying the bond, which leads to an increase in the money supply. Inflation crises emerge, when there is more and more money in circulation “chasing” fewer and fewer products and services. Prices will start to rise, because increasing production takes time (building factories, educating workforce, etc.). This will lead consumers and firms to expect higher prices in the future rising inflation expectations.

Let’s now assume that that there would be a financial crash with the economy heading into a recession. The Federal Reserve would enact another bailout of the financial system through QE-programs. The onset of a recession would mean that production capabilities would become hampered due to business bankruptcies (which can become very high in this cycle due to ‘zombie corporations’). As the pace of business bankruptcies accelerate, we would end up in a situation where demand suddenly spikes (due to increased money supply) while production simultaneously contracts. This could cause inflation expectations to rise rapidly leading to cycle of accelerating price rises.

If central banks in this situation were to continue to push more new money, through QE programs, into the economy, inflation expectations could potentially explode. Employees would start to rapidly increase their salary demands, while corporations that can would pass price increases through to their customers at an ever-faster pace to cover rising input costs and to remain profitable. With money printing continuing, and cycle repeating, an extremely rapid inflation would set in. The combination of massive increases in central bank credit (QE/bailouts) with declining production leading into exploding inflation expectations has been the main driver of historical episodes of runaway inflation also known as hyperinflation.

Any hint of inflation accelerating uncontrollably, would create a political outroar in the U.S. (at least) and it would not take long for the finger to point to central banks. At this point, the choice of central bankers would become: to let the economy implode or to risk hyperinflation. I am rather certain that central bankers would choose the former, either willingly or through force (political pressure). So, while I consider bailouts of the financial markets to be likely in the approaching recession and economic collapse, the road for ever-more pervasive central bank action can become blocked by rampant inflation.

Moreover, a legislation has been introduced in the U.S. to abolish the Federal Reserve. While this legislation is unlikely to go anywhere in the Congress, it will start to create pressure for the Fed to clean up their act. There are strong factions in the U.S. that have never accepted the creation of the Federal Reserve and they despise the massive role it has assumed in the U.S. economy. While the legislation is also unlikely to stop the Fed from bailing out the financial markets, again, it is likely to make it wary of not assuming any larger role in the economy, especially if inflation picks up again.

Many factors affect the current path of inflation. If the war in the Middle East commences, we can expect the inflation to shoot up regardless of the world economy heading into a recession. This would imply that central banks would be forced to rise rates into a recession and that their ability to enact major QE -programs to bailout the financial markets would become seriously hampered.

So, we have to acknowledge that, this time around, central bankers may not be “all-powerful”. This implies that when the collapse truly commences, there’s no certainty that the bailouts come and, if they come, they are likely to be limited and carry devastating consequences.

Let’s see how this plays out.

Disclaimer:

The information contained herein is current as at the date of this entry. The information presented here is considered reliable, but its accuracy is not guaranteed. Changes may occur in the circumstances after the date of this entry and the information contained in this post may not hold true in the future.

No information contained in this entry should be construed as investment advice. Readers should always consult their own personal financial or investment advisor before making any investment decision, and readers using this post do so solely at their own risk.

Readers must make an independent assessment of the risks involved and of the legal, tax, business, financial or other consequences of their actions. GnS Economics nor Tuomas Malinen cannot be held i) responsible for any decision taken, act or omission; or ii) liable for damages caused by such measures.

A bank is called a ’Primary Dealer’, when it’s permitted to deal directly with the government and/or the central bank.