Today, I will briefly comment on my forecasts for the price of gold and silver, which have failed, rather totally. The failure calls for a serious re-pondering of why the forecasts have failed so badly. The answer may be something we would not like to hear.

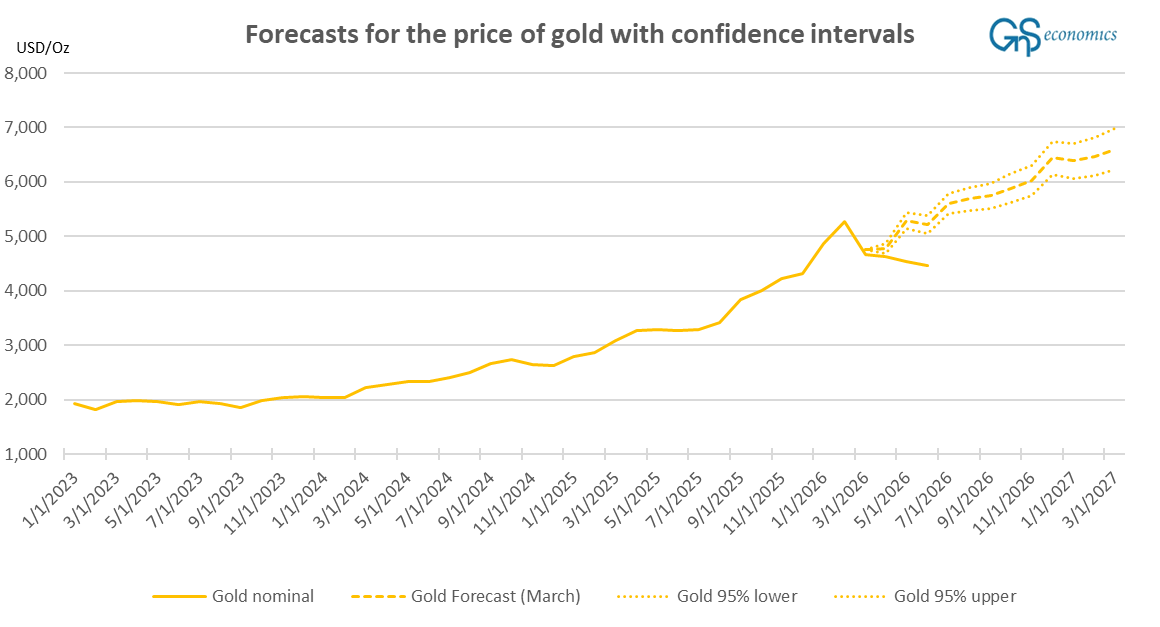

Figure 1 presents my (first) forecast for the price of gold from March, with 95% confidence intervals and realized monthly prices.

We can say that what is depicted in Figure 1 is a near-total failure of the statistical model forecasting-wise. My forecast assumed that the fall in the price of gold would stabilize and then head back up, but the opposite materialized.

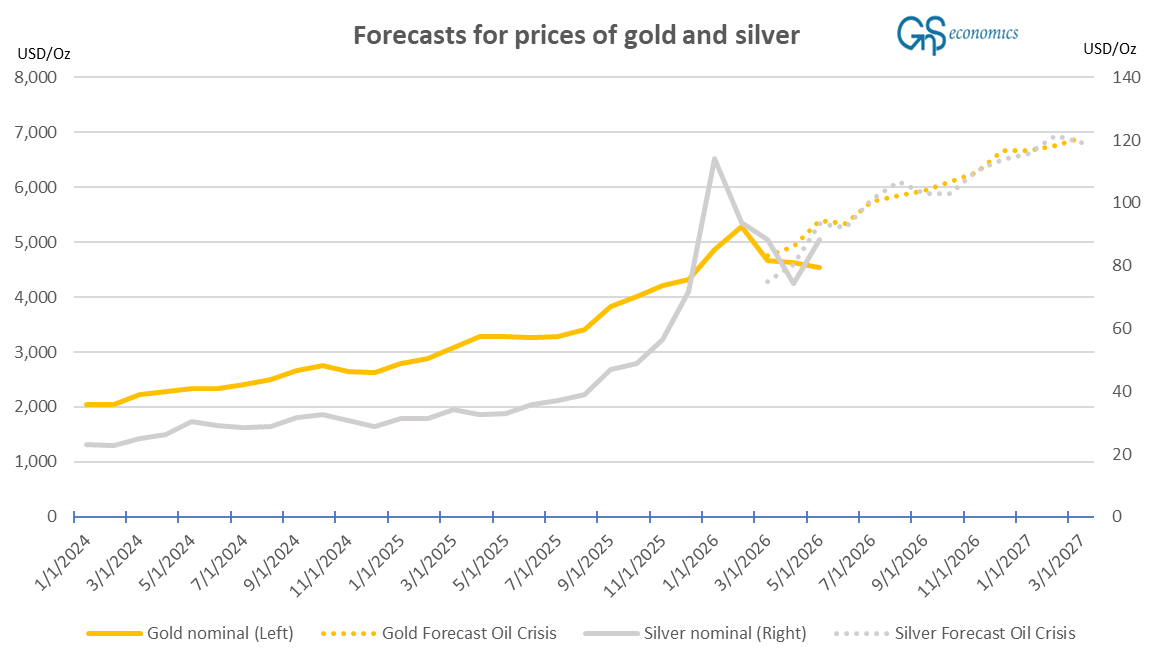

This failure implies that either there has been something fundamentally wrong in the model or that some crucial variable has been missing from it. Oil crisis scenario forecasts did not perform much better for gold, but they did ok-ish for the price of silver.

In Figure 2, you also see the major revision of the monthly price of gold from March to May. I’ve been using freely available data from MacroTrends, but I will have to change that. Market prices simply do not have revisions. Considering this, my price forecast for silver looks rather accurate, but we have to monitor it for a few months to know for sure.

Returning to the price of gold. The model relied heavily on the assumption of the stochastic trend providing relevant information for forecasting. The question I need to ask is whether the parameters (like the lag structure) of the model were such that it was able to correctly estimate the (possible) underlying stochastic trend.

The fact that the silver price forecast looks relatively accurate hints that there would not have been a problem with the model per se, but that some other variable, which the model did not know how to predict with the information in the stochastic trend, drove its price from March to May. We can assume that the stochastic trend process is capturing the market dynamics, which implies that the gold price behaved contrary to the market dynamics stored in the stochastic trend. In other words, some other factor than market dynamics drove the price of gold in March, April, and May. What could this be?

I honestly do not know, but considering the above and the fact it has not behaved like it did in the previous Middle East oil crisis, it indicates market manipulation. We naturally cannot know this for sure just based on the above, but something is “off” with the price of gold.

Tuomas

Disclaimer:

The information contained herein is current as of the date of this entry. The information presented here is considered reliable, but its accuracy is not guaranteed. Changes may occur in the circumstances after the date of this entry, and the information contained in this post may not hold true in the future.

No information contained in this entry should be construed as investment advice nor advice on the safety of banks. Neither GnS Economics nor Tuomas Malinen can be held responsible for errors or omissions in the data presented. Readers should always consult their own personal financial or investment advisor before making any investment decision or decision on banks they hold their money in. Readers using this post do so solely at their own risk.

Readers must assess the risks and legal, tax, business, financial, or other consequences of their actions. GnS Economics and Tuomas Malinen cannot be held i) responsible for any decision taken, act, or omission or ii) liable for damages caused by such measures.