China slowdown

We have been China “bears” for around four years. In this post, I’ll detail the reasons why and explain why the slowdown of the Chinese economy, which is on its way, threatens the feeble recovery of the world economy.

In September 2017, we wrote:

Since 2008, the global economic expansion has been driven mainly by one country: China

This is alarming as the economic growth in China lays on a labile ground.

In addition to a massive global asset bubble, the unorthodox central bank policies have created a “zombie economy”, where growing share of companies survive only through cheap credit.

In April this year, we warned in our Deprcon Outlook that: Beijing has signaled that they will start to rein-in credit creation. The next few months will show whether this happens or not.

Beijing has a strong grip on its banks. It can effectively order them to increase or decrease lending in a ‘command and control’ manner, which means that when Beijing signals that it will limit credit creation, it tends to occur.

So, the “threat” made by Beijing, unsurprisingly, materialized (see the figure at the end of the post), and now we have started to see its effects in China.

What does the slowdown of the Chinese economy mean for the global economy?

The lead of China

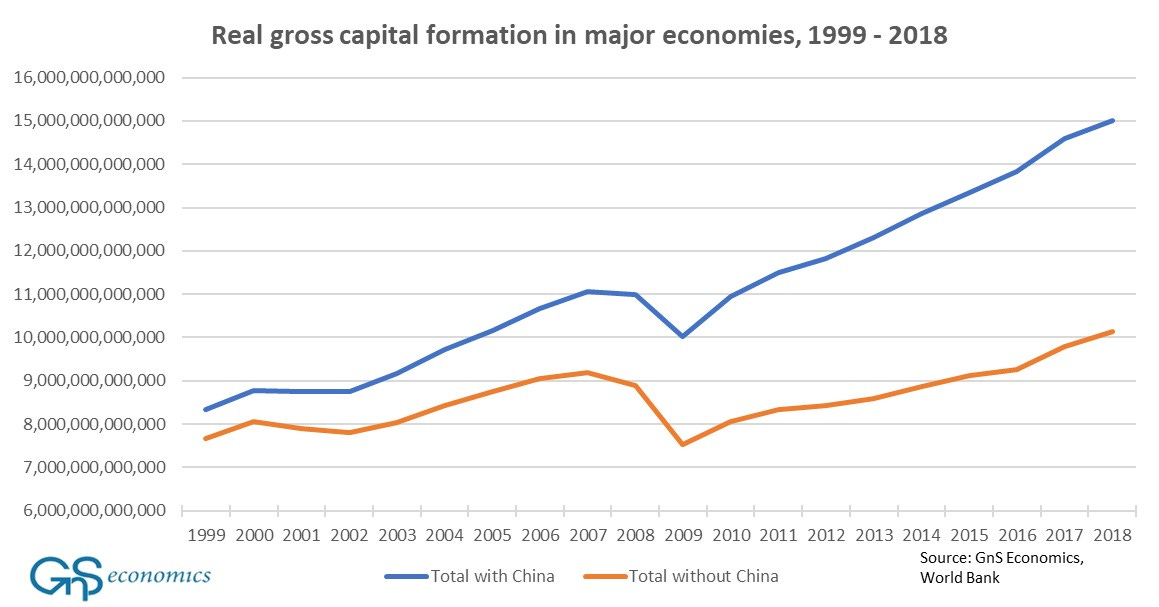

Like we explained in Q-Review 3/2017, China has driven global growth since around 2009. This is visible, for example, in the gross capital formation of major economies.

Astonishingly, China has accounted around half of the growth in gross capital formation in major economies (including the eurozone) since 2009. This is why we can say that China has been driving the global economy.

Therefore, its no surprise that during the past 12 years, the Chinese credit-cycle (i.e. leveraging/deleveraging of the economy) has led the global economic cycle by around 2-4 months.

This time around the reopening of economies has disrupted this “economic law”, but unless Beijing turns back to increasing debt-stimulus, the global economy will start to sputter.

China in trouble

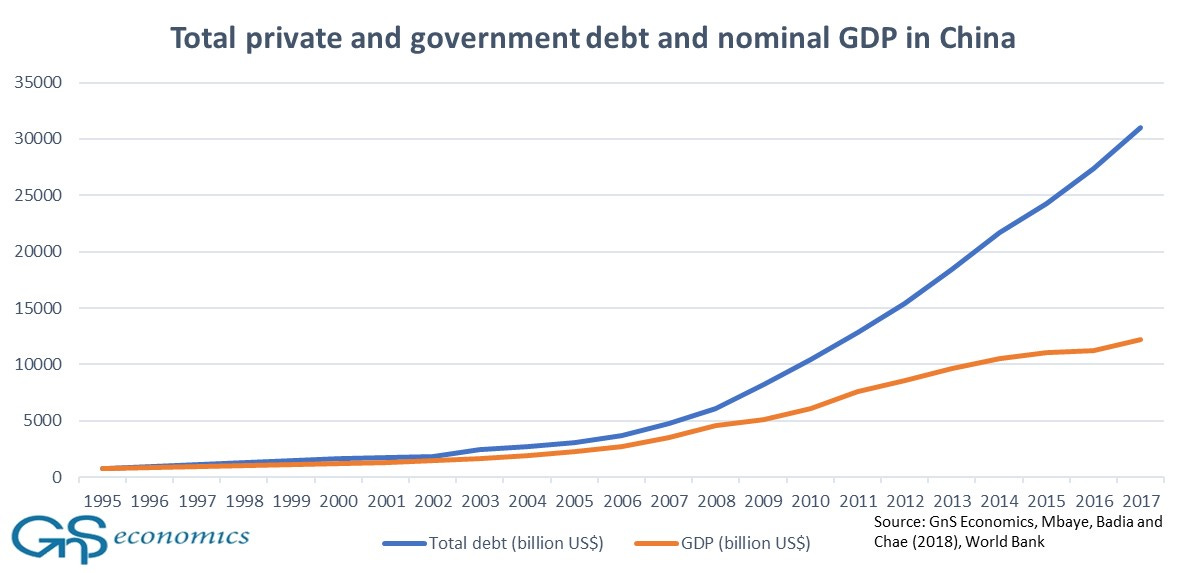

China’s economic troubles can be summarized with three figures.

The first of them presents the estimated total level of (government and private) debt and the gross domestic product.

It’s very clear that China’s economy is not in a sustainable path. More and more debt is needed for the economy to grow.

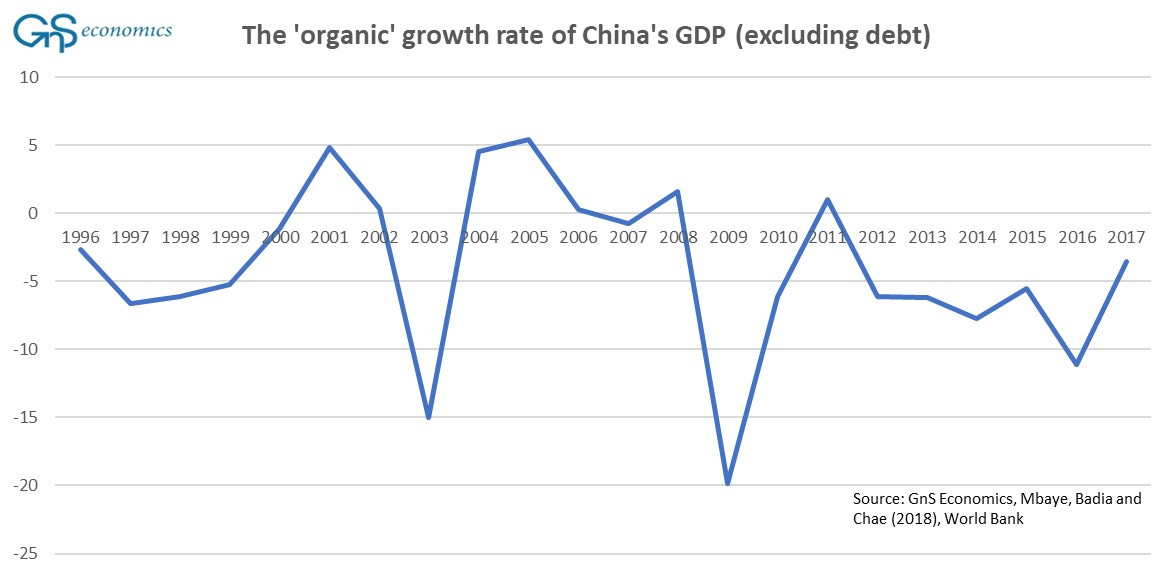

If we deduct the growth of debt from the growth of GDP, China’s GDP growth-trajectory looks very different.

Exlucing the growth of debt, Chinese economy actually declined between 2012 and 2017. The same trend has been likely to have been continued after, but China’s problems do not end there.

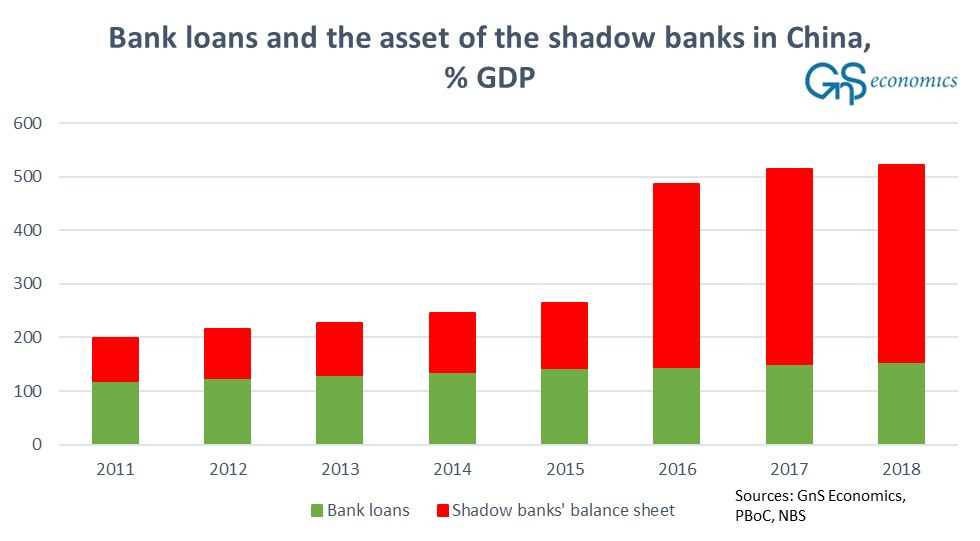

Next figure presents the bank loans in commercial banks and the size of the balance sheet of the shadow banking sector in China.

The massive increase in the balance sheet of the shadow banking sector in 2016, is a result of a ‘astronomical’ debt-stimulus run through the unregulated financial institution also known as “shadow banks”. We have explained the development of the shadow banking sector in more detail in this blog.

As unregulated entities, shadow banks can give out riskier loans and operate with very low capital buffers. Simplified: the higher the share of shadow banks in the economy, the more risky (and fragile) the financial sector, and the economy, are.

So, if we exclude the growth of debt, Chinese economy has not grown in years. Moreover, her financial sector is massively bloated and it is dominated by risky shadow banks.

To put it bluntly, Chinese economy is a ‘debt bomb’ waiting to explode.

China slowdown; a threat to the world economy

In August, the Purchasing Managers Index (PMI) of the non-manufacturing sector of China plunged into contraction with a pring of 47.5 (every value under 50 signal a contration). China Caixin PMI of the manufacturing sector, which is a private survey, recorded a print of 49.2 for August.

Many want to blame local coronavirus outbreaks for this slowdown, but the more likely explanation is the diminishing debt-stimulus in China. As you can see below, the aggregate financing of the economy has been notably smaller than past year. Beijing thus kept its promise from late March. It’s trying to delever again.

The simple fact is that, as shown in the “Organic growth rate” -figure above, that the Chinese economy cannot grow without massive debt-stimulus and when it diminishes, the economy will falter, which is now happening.

This is should worry us, because the global economy cannot escape from the slowdown of Chinese economy for much longer. The weight of China in the global economy is just too large. Chinese economy has been and continues to be the driver of the world economy.

Alas, if Beijing does not quickly turn the ‘credit levers’ back up, prepare for a rough fall ahead!