Inflation in 2023

I kept a vacation for a week. I visited Pallastunturi and Levitunturi in the north-western part of Finland (west Lapland). It was a much needed break from the ‘doom-and-gloom’ of past year. I skied (downhill), snowbiled, wondered in the wild and met interesting people.

We had some intriguing discussions on the economy and the Russo-Ukrainian war in the panoramic sauna of Panorama hotel Levi. This, having serious discussions in the sauna, is a Finnish tradition, even though this time most of the discussions took part in english with tourists and people working with the Porsche Ice Experience (no advertisement).

Discussions revealed, again, the fact that majority of people tend to be wholly unprepared for the worst-case options. I, on the other hand, have been pondering the worst-case options all my adulthood. In part, this due to the passing of my father, when I was just two months old. My life started with a massive adverse shock. My first memory of the economy was the early 1990’s banking crisis and depression of Finland. That shooked my world (less then others, though) and made me understand how important the economy and preparation for its adverse outcomes, to uncertainty, is.

Future uncertainty can only be met with the help of scenario forecasting. The concept of it has turned to be relatively difficult to explain to people, almost completely regardless of their educational background. Academic economists and mathematicisians I’ve worked with have naturally understood the concept, but it does require a rather high level of abstract thinking. This is attainable to everyone, I am sure, but it tends to require a bit of work and especially rearranging of one’s own thinking.

Now, we (the world) are in a phase, which requires a high level of abstract thinking, if one wishes to understand where we are heading.

We laid the principles for the road ahead in our scenario forecasts published in the last days of 2022. Their range could hardly be any wider. The worst-case scenario essentially established a road to World War III. The best-case scenario, naturally, painted a road to peace and properity, though an economic crash, though.

I am rather certain that the road we will take will emerge during the next few months. Thus, I decided to use the first weeks of this year to map, where I think we are heading.

I start with painting the inflation picture going forward. In the next posts I will dwell on the economic prospects and publish an update to my worst-case scenario concerning the Russo-Ukrainian war.

Let’s start with a look to the energy markets.

The energy-road ahead

This section can be started with a positive note.

The very mild winter in Europe has clearly diminished the risk of another energy price shock and rolling blackouts. That said, we need to remember that we are only in the first half of January with two full winter months to go. Looking a bit further, uncertainty grows quite notably.

Gas imports to Europe have collapsed from 2021. They kept up till October, but after that a growing divergence, in imports, between 2021 and 2022 emerged. Like I mentioned earlier, global liquified natural gas, LNG, market is likely to be maxed out till 2025/2026. If winter continues as a mild one, we should be ok-ish, but if not, troubles emerge.

In any case, the fact that while natural gas imports have collapsed, gas storages, e.g., in Germany are being filled mid-winter, no matter how mild, implies that consumption has fallen drastically. This means closures of factories and halting of production, i.e. de-industrialization, has been at ‘full-swing’ late past year. First repercussion of this will be felt during this quarter (more on this in the next post).

Effectively, the same applies to hydro-reservoirs in the Nordpool area. At the end of 2022, they were clearly below their long-run average. Now, also concerning them, everything depends on the weather.

As an interesting turn of events, Thierry Mariani, a French deputy of the European Parliament, stated that the EU will start to negotiate with Russia on gas deliveries within the next few months. This would be a welcome development, as it would entail a truce and likely peace in Ukraine. Let’s see what manifests (I fear the worst, i.e., escalation).

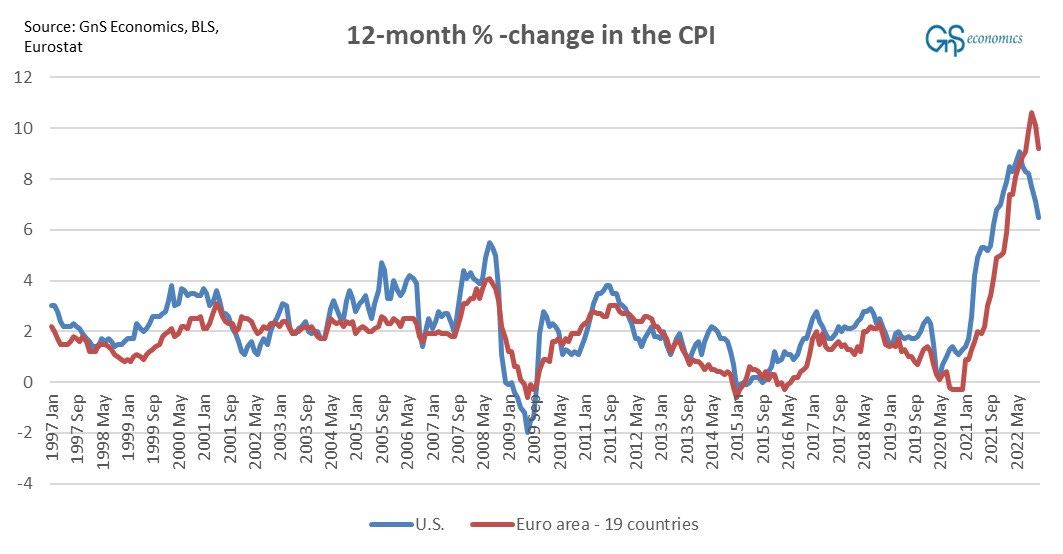

The inflation drop

Inflation moderated during the end of 2022. In the U.S., the pace of annual inflation decelerated to 6.5% in December. But, where is it heading?

In the U.S., the NFIB small business survey shows a noticeable decline in their pricing plans. However, they also seem to be most afraid of inflation. This is a paradox, which can be explained only through massive uncertainty SME:s see concerning the path forward. And they have good reasons for this.

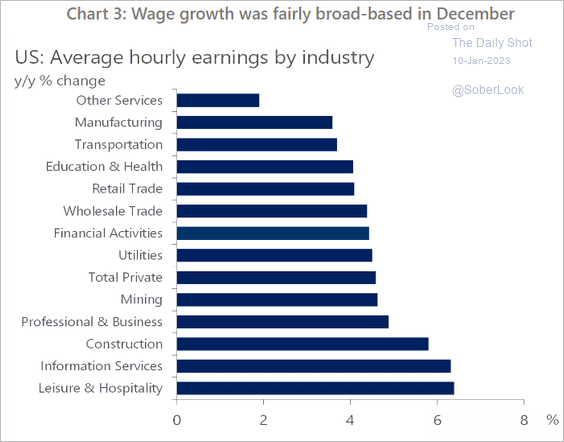

Wages are rising rapidly in the U.S. in all sectors. This implies that while the peak is currently past us, inflation is likely to remain high, and more shocks may follow.

Food inflation is getting out of hand in the U.S. For example, the prices of eggs have skyrocketed in the U.S. All policies that hamper agricultural production naturally aggravate the issue. Policies enacted to close down “peak polluters”, from which most of are farms, are rather unfathomable considering that food inflation and shortages are an actual threat. Yet, the biggest hurdle of farmers currently face are the rapidly rising costs of production.

We see also cooling of inflation in the Eurozone, which has arisen mostly from the easing of energy prices. However, this may become very volatile again in the coming months, driven by weather and possible adverse developments in Ukraine (more on this later). We thus cannot have a sigh of relief, yet.

Economy naturally plays an important role on how inflation will develop, and I will return to it next week. I will also continue to sketch my worst-case scenario on the Russo-Ukrainian war in the coming days/weeks.

Disclaimer:

The information contained herein is current as at the date of this entry. The information presented here is considered reliable, but its accuracy is not guaranteed. Changes may occur in the circumstances after the date of this entry and the information contained in this post may not hold true in the future.

No information contained in this entry should be construed as investment advice. Readers should always consult their own personal financial or investment advisor before making any investment decision, and readers using this post do so solely at their own risk. Readers must make an independent assessment of the risks involved and of the legal, tax, business, financial or other consequences of their actions. GnS Economics nor Tuomas Malinen cannot be held i) responsible for any decision taken, act or omission; or ii) liable for damages caused by such measures.

Can somebody help square this inflationary outlook with this M2 vs other deposits chart? https://twitter.com/NathanDallon/status/1615084548399792150?s=20