The Credit Recession

The non-recovery of the U.S. economy

Issues discussed:

The ongoing credit recession stands in stark contrast to the no-landing, or no-recession, narrative for the U.S. economy.

Bank lending to corporations has not recovered signaling a recession among the small and medium-sized enterprises.

Investors gorging on junk bonds, with the assumption no U.S. recession, are risking catastrophic losses ahead.

Tensions in the Middle-East are extremely high.

The strong economy that wasn’t

The single most important indicator on the strength of an economy is credit demand. This is because it defines investments to productive capital and real estate, determining the future growth potential of the economy. Credit creation, by commercial banks, also is the main source of new money entering the economy. If credit is not demanded, and banks thus do not lend, a credit recession appears, which will start to eat to the future growth potential of the economy leading it eventually to fall into a recession, unless new money (credit) is added to the economy by other means (e.g., through central banks and/or governments).

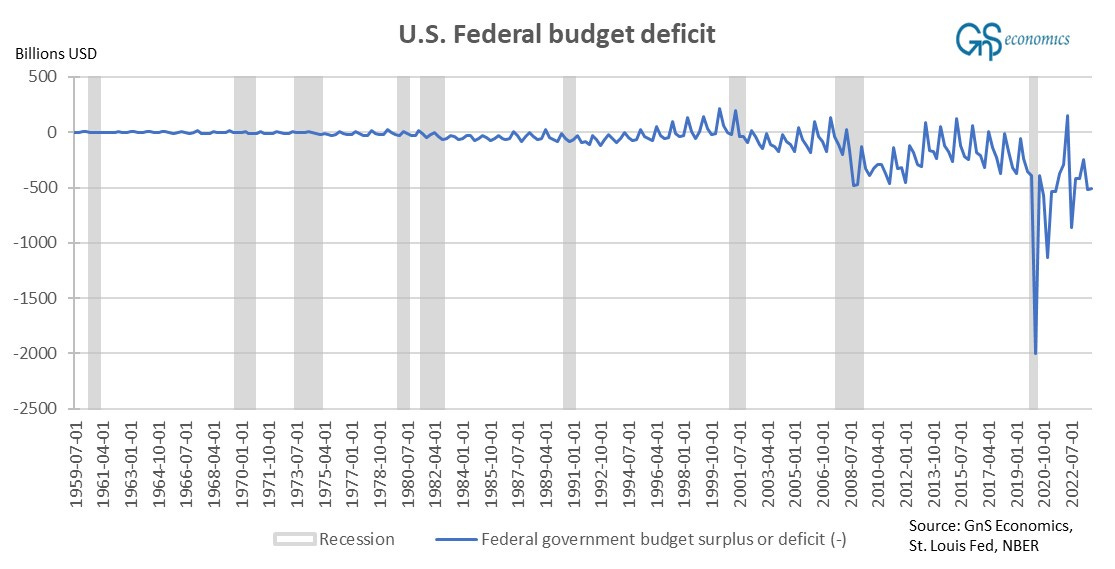

It’s important to note that these are not substitutes. To commercial banks, lending is a business, while central banks and governments try to manipulate the system with their money (credit) creation. This means that while CB/government money creation (lending) can support the economy, it tends to be unsustainable and create all kinds of “perversions” into the economy (I’ll write about this important difference in more detail later). What we are now seeing in the U.S. is utterly unsustainable debt (fiscal) stimulus by the Biden administration.

Like we noted in the March Deprcon Outlook of GnS Economics, this (unsustainable fiscal stimulus) is what is carrying the U.S. economy with the interest expenses at an exponential trajectory. This quite directly implies that this stimulus has not long to run. The picture turns even darker, when we observe the loan demand in the U.S. economy.

Demand for credit card loans is sub-par, and clearly at recessionary levels. In Q1 this years, there was a notable decline in percentage of banks reporting declining demand for consumer loans, excluding credit card and auto loans. However, I am suspecting that this was created by the false optimism of the U.S. economy and consider that it will be short-lived. Demand for CRE loans continues to hover at abysmal depths.

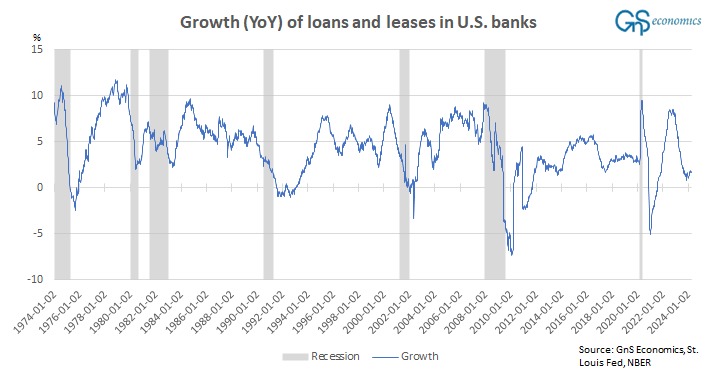

When we observe the (Y-o-Y) growth of loans and leases of U.S. banks, we notice that they continue to hover at recession levels. I expected to see an improvement during February and March, due to improved mood among consumers and expectations of rate cuts, but this failed to materialize almost totally as shown by the figure below. This enforces the message of loan demand, i.e., that the U.S. economy is nearing a credit recession.

Humpty dumpty on the wall of credit

Keep reading with a 7-day free trial

Subscribe to Tuomas Malinen on Geopolitics and the Economy to keep reading this post and get 7 days of free access to the full post archives.