What will the central bankers do?

What will the central bankers do?

With interest rates, and for their survival (free)

I wish to thank Dr. Peter Nyberg for his insightful comments and suggestions. Remaining errors are my own.

Issues contributed:

The losses of central banks and their repercussions.

The ‘death spiral’ of the ECB.

How high will the interest rates go and for how long?

The two probably most failed economic forecasts for the past three years have been: inflation and interest rates. We have been warning for quite some time that at some point interest rates will shoot up. Now it has happened, but where are they heading next?

In March 2021, we warned on the coming inflation shock and in June/July 2021 on the “persistence” of inflation. In both occasions we iterated that the hastening inflation will put central bankers in a very difficult spot, as they would be forced to go against the needs of inflated asset markets, which require cheap money, i.e., low interest rates to stay afloat. At present, of course, this situation is made even more difficult by politicians' perceived need for financial expansion at a time when inflation is high.

However, there was also a bigger issue, which was almost completely overlooked, until recently. In the March 2021 Q-Review report, we noted that:

Bonds show as assets, while central bank reserves show as liabilities [in the CB balance sheet]. Now, if interest rates on the reserves rise, while the price of the bonds fall, the central bank will start to incur losses that can eat through its capital. This would either force a recapitalization of the central bank by a finance authority, a Treasury, or force the central bank to operate with negative equity.

This process is naturally aggravated by the mark-to-market accounting, where the value of assets are marked to daily values compared to their purchase price. Recently, the Swiss National Bank, SNB, posted a loss of (rather unfathomable) SFr142.4 billion for the first nine months of 2022 (around $153 billion). It’s the biggest loss of SNB during its 115 year existence, and it arose from the falling stock (especially NASDAQ as the SNB hold/held a lot of stocks of technological companies) and bond prices and from the slide of the value of the Swiss franc.

The Treasury of the United Kingdom re-capitalized the Bank of England, BOE, by £828 million during the third quarter this year, with an expectation that “these payments would continue for the foreseeable future“. The similar thing occurred in the U.S., where the net income by the Federal Reserve to the U.S. Treasury turned negative. Effectively, this implies that the Treasury is re-capitalizing the Fed, while the losses are written down as a deferred asset, which the Fed expects to cover after it turns profitable again. However, when this would to occur, is a complete mystery taking into account the massive balance sheet of the Fed (consisting mostly on U.S. Treasuries).

The Federal Reserve is conducting the asset roll-off, or QT, program in a way to avoid extra losses. Essentially this means that the Fed let’s a certain amount of Treasuries mature every month so that the Treasury pays the principal and the Fed does not purchase a new bond to replace it. This does not create a loss as the asset (bond) has been “sold” with its purchasing price (+ interest). Still, the mismatch between rising interest on reserves and falling bond prices (higher yields) holds. Therefore, the Fed is likely to incur a loss for a long time.

However, the true ‘problem child’ in the genre is the European Central Bank.

The European ‘Cabal’ Bank

The European Central Bank is essentially a “community” of the 19 national central banks of the European common currency (euro). While national central banks are financially operating under the cover of their respected finance ministries, the ECB itself has no such cover. This, quite straight-forwardly, implies that there’s currently no line of direct re-capitalization of the ECB, except through their member national central banks, nor tax-payer support.

The ECB states that its losses would be covered by the national central banks and, if that is not enough, through the deferred asset, which the ECB defines as: “Any further amount may be recorded on the ECB’s balance sheet, to be offset against any net income received in the future.“ However, unlike the Fed, relying on such a practice is much more problematic for the ECB.

We noted in Q-Review 3/2019 that:

If, alternatively, a central bank continues to operate with negative net worth and/or without acknowledging its losses, it will interfere with its own monetary management (the setting of interest rates) and eventually jeopardize its independence and credibility. What this means as well is that financial market participants cannot be sure whether a central bank is conducting monetary policy according to its mandate or in an effort to cover its losses.

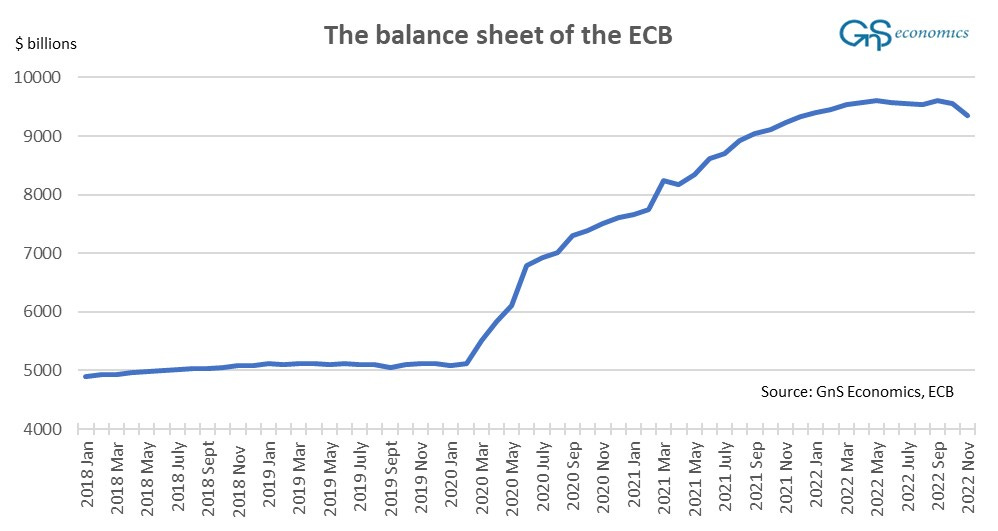

The question is, how credible of an “inflation fighter” the ECB will be, when its losses mount for each step it rises its interest rate? The massively bloated balance sheet of the ESCB (European System of Central Banks) guarantees that the losses of the ECB are likely to be extreme making the funds national central banks have gathered to cover it (€116bn of provisions and €113bn of reserves) rather small.

Will the markets or the banks trust the ECB after losses starts to mount forcing the Bank to operate with (large) negative equity? We simply do not know.

Thus, the tough tone of speeches of President Christian Lagarde should be taken with a ‘grain of salt’, as each interest rate rise undermines the credibility of the ECB.

What comes to the possible re-capitalization of the ECB, one might say that the issue is rather complicated. Again, from Q-Review 3/2019:

While losses of the ECB from its bond holdings would constitute a direct breach of Article 123, any possible recapitalization of the ECB would breach Article 125.

We argue that the recapitalization of the ECB, e.g., by the EU would imply acknowledging that it had given credit lines to European institutions and governments thus breaching TFEU (Treaty of the Functioning of the European Union) Article 123. Alternatively, recapitalization of the ECB by national governments would assume mutual fiscal responsibility on government debt breaching TFEU Article 125.

More importantly, the ECB has “conspired” itself to its current problems. That is, without QE -programs, which were most likely aimed at keeping borrowing costs of some Eurozone government low thus breaching the Article 123, the ECB would not be in this mess. They reap what they have sown.

Thus, I consider the re-capitalization of the ECB rather unlikely. This means that it will at some point start to operate with negative equity, and then we'll see how markets react.

Interest rates: How high and for how long?

The mounting losses of central banks will almost surely become a political issue at some point. With the government revenues dwindling due to recession, and especially after their collapse in the upcoming economic crisis, questions will be raised whether public money should be used to uphold central banks, who essentially “dug their own hole”. This is, of course, one obvious reason to try to solve the issue using bookkeeping magic rather than recapitalization.

It’s relatively easy to construct a path of public discourse eventually questioning the whole existence of central banks. We return to this in the scenarios published in the Derpcon Outlook next week.

Yet, it’s likely that the political pressure of central bank losses has and will continue to affect on the behaviour of central bankers in addition to the risk of an outright financial market collapse. However, their credibility would take a massive hit also, if inflation would truly get out of hand. Everything would naturally be well if inflation would simply come down. However, as I’ve argued previously, this looks unlikely.

There’s thus the possibility that they will “go down in flames”. That is, it’s possible that central bankers rather sow their own demise rather than let themselves go to history as the ones who completely failed their most important mandate, i.e., price stability. Assessing the path of rate hikes is thus a massively complicated maze of factors affecting inflation, the economy, financial markets and the political landscape.

Thus, at the current time, the path of interest rate hikes and other central bank actions (QE/QT) remains essentially unforecastable, at any reasonable margin. There are simply too many factors, ranging from geopolitical ambitions to human psyche, at play. However, we can consider 7% as something of a threshold after which everything simply falls apart in the markets and in societies. At current time, I consider this as the upper-bound.

So, my advice is not to trust anyone, who thinks he/she can say how high interest rates will go and for how long they will stay there. But, as I also noted previously, we are likely to have exited from the long period of low interest rates. This would be good to factor in to any longer term plans.

Disclaimer:

The information contained herein is current as at the date of this entry. The information presented here is considered reliable, but its accuracy is not guaranteed. Changes may occur in the circumstances after the date of this entry and the information contained in this post may not hold true in the future.

No information contained in this entry should be construed as investment advice. Readers should always consult their own personal financial or investment advisor before making any investment decision, and readers using this post do so solely at their own risk. Readers must make an independent assessment of the risks involved and of the legal, tax, business, financial or other consequences of their actions. GnS Economics nor Tuomas Malinen cannot be held i) responsible for any decision taken, act or omission; or ii) liable for damages caused by such measures.

This question seems to be relevant these days. Why those stress tests didn't find banks like Silicon Valley and Signature? Will those tests fail e.g. in Eurozone or Asia too? BR JKi