2023

The year everything comes to head?

Issues contributed:

Revisiting the state of the global financial sector.

The ‘stealth pivot’ of the Federal Reserve.

The big “If’s” of 2023.

The coming war economy?

Past five years have been rather grueling for a crisis forecaster. Like I mentioned before, I (we) had a great epiphany in early 2017, when we noticed that the global financial sector had not recovered from the Panic of 2008. This was no surprise as academic research has asserted that it takes about 10 years for the banking sector to recover from a financial crash.

In March 2017, we wrote:

The crisis of 2007 - 2008 reversed the trend of financial globalization, which has undermined global growth. The pull-back in financial globalization has been masked by central bank-induced liquidity and continuous stimulus from governments which have created an artificial recovery and pushed different asset valuations to unsustainable levels. This implies that we live in a “central bankers’ bubble”.

We were somewhat ridiculed of this, but that is the ‘crux’ of a forecaster. When you are constantly few months to few years ahead of most, you become a laughing stock among those, who are unable to see, where we are heading. Even more so, if the vulnerabilities you have observed fail to materialize as a crisis, because of the actions of authorities.

This became a norm in the global economy after the 2008 crisis. Politicians and especially central bankers ‘rode’ to the rescue of the global economy and financial markets every time implosion appeared imminent. Last time this occurred was in late September, when the Bank of England bailed out U.K. pension funds, and in early October, when the Swiss National Bank (SNB), with the help of Federal Reserve and the Saudi National Bank, saved the venerable swiss banking giant Credit Suisse. The onset of a global banking crisis was averted, yet again.

The question every economic forecaster is currently asking, is what happens in 2023? Like I and we have been touting all through the fall, major economic tectonic plates are moving below the surface. Many have felt the tremors, but decided to ignore them.

In this piece I will go through the main ‘burning points’ and speculate on the timing. Our three scenarios for the future paths of the global economy will be published at the GnS Economics Newsletter on Friday.

The state of the global financial system?

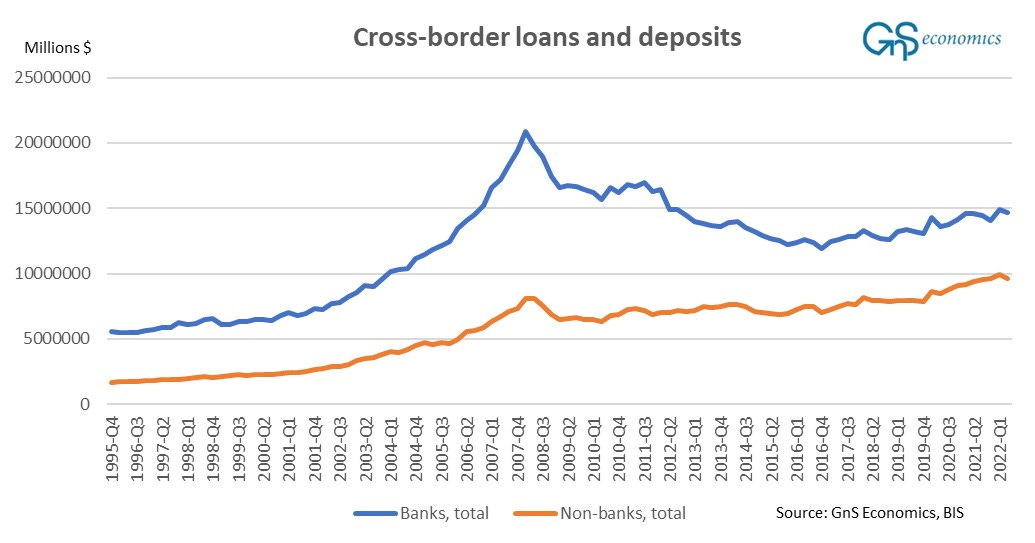

During this fall, I have kept an eye of the global liquidity statistics. Now, I decided to re-visit the cross-border banking statistics, from where we drew our early 2017 warning.

The figure above, on cross-border lending of commercial and ‘shadow ‘ banks, shows two things.

First, there has been a mediocre recovery in financial globalization and global banking since after (around) Q4 2016. This shows as a growing trend of cross-border loans and deposits of banks since early 2017.

The second conclusion is not so encouraging. The figure above shows that the cross-border lending activity by non-banks, i.e., by financial institutions that are less regulated as commercial banks, known as ‘shadow banks’, has grown even above the 2008 peak, while that of commercial banks has diminished. This implies that a considerably larger share of the global financial system is being controlled by less-regulated entities.

As explained in my previous post, shadow banks are likely to take higher risks and operate with higher leverage than commercial banks. This has made the global financial system fragile and prone to a sudden drying up of liquidity and collapse.

The ‘stealth pivot’ of the Fed?

Usually, global market liquidity (credit) diminishes with the asset roll-off (QT) programs by the central banks. This time, however, it seems that central bankers have learned their lesson, somewhat.

Daniel Lacalle, a chief economists at Tressis, recently tweeted a chart on global USD liquidity. It shows a remarkable rise in global money (USD) supply since late October. This is likely to be a result of the near-collapse of the U.K. pension funds and Credit Suisse. Central bankers realized what was happening, got scared and decided to find ways to push liquidity into the financial markets, while running a QT -program. As Michael Howell, a managing director at Cross Border Capital, puts it in his FT piece:

…quantitative easing programmes by central banks to support markets are impossible to reverse quickly because the financial sector has become so dependent on easy liquidity. The very act of quantitative tightening creates systemic risks that demand more QE.

This is something we have been warning for a while. In our report on QE/QT, published in March 2018, we wrote:

It is likely that it will take some time before the effects of QT move through the system, but ultimately they will. The losses on bonds and especially on the high yielding products will slowly start to cascade. The balance sheets will deteriorate and some small runs, mostly unnoticeable by the general public and the media, will start to appear in the hidden corners of the financial markets. But, after the (unknown) critical point is reached, the cascading losses will ignite a run in one of the major asset markets, the most likely candidate being the high yield (junk bond) market.

This is what almost, again, occurred in late September/early October.

But how have central bankers pulled this (increasing money supply) off even with the QT of the Federal Reserve?

Mr. Howell provides an explanation. First, People’s Bank of China enacted forceful liquidity operations in November, similarly as it did in early December 2018. Secondly, the Fed has used “other liquidity means” to balance the effects of QT. As explained by Michael:

But net liquidity provision, benchmarked by moves in the Fed’s “effective” balance sheet, has remarkably risen in six of these weeks. In fact, the Fed added an impressive $157bn to US money markets through its operations.

We can call this as the ‘stealth pivot’ of the Federal Reserve, through “other means”.

Essentially the Federal Reserve is engaged in a ‘surgical operation’, where it tries to stave off inflation, while preventing the financial markets from collapsing. Needles to say that such a maneuver has never been tried before. Thus, we are, again, at uncharted waters.

The big “If’s” of 2023

In my posts over the course of this fall I have documented:

The fragility of the European financial system,

The many phases of the currently ongoing energy crisis leading to the de-industrialization of Europe,

The threatening collapse of global liquidity,

Interest rate hikes crushing households and corporations,

Major issues faced by central bankers, and

The possibility of a nasty “winter surprise” in Ukraine.

I consider these as the current building blocks of the ‘perfect storm’, we first warned in December 2017. Essentially we have a never-before-seen number of factors threatening the global economy and the global financial order.

The problem here is that majority of them are driven by political decisions (hence “big if’s”). Moreover, the whole process of collapse can be initiated by pure political decisions, with one possible major trigger being a winter offensive of Russia in Ukraine.

This means that forecasting of such developments (the “big if’s”) and thus the arrival of the crisis, is cumbersome to the point of extremity, and solvable reliably only through scenario analysis and forecasting.

Timing?

Back in 2017, the timing of the onset of a market turbulence and possible crash were relatively easy to forecasts. In the December 2017 Special Report, we wrote:

We recommend keeping a close eye on the central bank balance sheets, commodity prices (especially aluminium and nickel where the role of China is the largest), high-yield bond markets and all news from China.

Major changes in these, especially in the global CB balance sheet, foretold the market turbulence in October-December 2018 and the near-collapse of the repo markets in September 2019. This year it foretold the near-collapse of the U.K. pension funds. Now, however, it seems that central bankers are trying to avoid a major financial event by adding liquidity through “the backdoor”.

Yet, liquidity alone cannot support the markets, which means that fiscal stimulus is required to build an upward momentum in the economy and markets. Beijing has been reported of announcing a large stimulus programme. The stimulus program Beijing announced in May, was actually used just to fill the funding gap of the government. Like we’ve been detailing, the aggregate financing to the Chinese economy has fluctuated heavily throughout the year. Soon, we will probably know how forcefully Beijing is able stimulate her heavily indepted economy.

Currently, I think that ‘everything’ depends on what happens in Ukraine. I do fear that a major Russian offensive, possibly a ‘blitzkrieg’ crushing through Ukrainian lines and even to Kiev could start a chain reaction, where a run to safety in the asset markets would combine with renewed prices pressures of energy and food and deepening downturn in the global economy.

This could entail a change to a “war economy" across the western hemisphere. Central banks could (would) be leashed to serve the needs of government financing, and Treasuries would enact another round of massive fiscal spending. Inflation targets would most likely be dismantled. This, escalation and rearmament is a way to avoid the crash and crisis, unfortunately, as it has been so many times in history.

So, forecasting the onset of the collapse, or other major turning point, has turned into a political-meteorological exercise. Weather is likely to play a role in what happens both in Ukraine and with the gas storages of Europe. If there’s a Russian winter offensive, it will most likely commence after 1) a sufficient number of conscripts have been trained and moved into the battlezone and 2) the gound freezes to carry tanks.

This implies that the “crush point” is likely to arrive in January or February, when the winter usually arrives to central-Europe. And at that point, the direction of our world and economies will be decided. I hope that we never arrive to such a point, but it’s starting to look worryingly likely.

But, like I mentioned above, it’s impossible to form a comprehensive picture of such a major, high uncertainty event without scenario analysis. We’ll return to these on Friday in the GnS Economics Newsletter.

Keep preparing.

Disclaimer:

The information contained herein is current as at the date of this entry. The information presented here is considered reliable, but its accuracy is not guaranteed. Changes may occur in the circumstances after the date of this entry and the information contained in this post may not hold true in the future.

No information contained in this entry should be construed as investment advice. Readers should always consult their own personal financial or investment advisor before making any investment decision, and readers using this post do so solely at their own risk. Readers must make an independent assessment of the risks involved and of the legal, tax, business, financial or other consequences of their actions. GnS Economics nor Tuomas Malinen cannot be held i) responsible for any decision taken, act or omission; or ii) liable for damages caused by such measures.

The mentioned war economy could boost TFP, or at least increase production.