Peak inflation?

Or not

Issues contributed:

Inflation has become ‘anchored’ in the U.S., and only draconian interest rate hikes and/or recession can bring it down.

Forecasts on European energy situation are very worrying, and we are just entering the “phase II” of the energy crisis.

Globalization is reversing and this is likely to end the era of low inflation and interest rates.

Some analysts and central bankers are arguing that the “peak inflation” is either in or it’s close. Is there any merit in their arguments?

It’s true that inflation has eased, somewhat. In France the harmonized consumer price index, or HCPI, grew at an annualized pace of 7.1% in November. The consumer prices are expected to have risen “only” by 10% (annualized) in Germany in November. In the U.S., inflation has eased a bit more.

So, are we in the “mend”? I think not. In this post I will document, why the peak-inflation -crowd is likely to be mistaken.

Let’s start with a recent summary of Bundesnetzagentur, the German gas authority. On 8 December 2022, the institution stated that:

Wholesale prices are fluctuating greatly and have recently seen a slight decrease. Businesses and private consumers must continue to adapt to a significantly higher price level.

Do I need to write any more? ;)

The German gas authority warns citizens and corporations to prepare for a considerable higher prices in the near-future. It also warns that temperatures are forecasted to be 2.38 celcius lower this week, and so “significantly higher consumption is expected“. Alas, like I wrote earlier, winter is here and now the “Russian energy roulette” truly begins.

But, let’s take a closer look at where we stand.

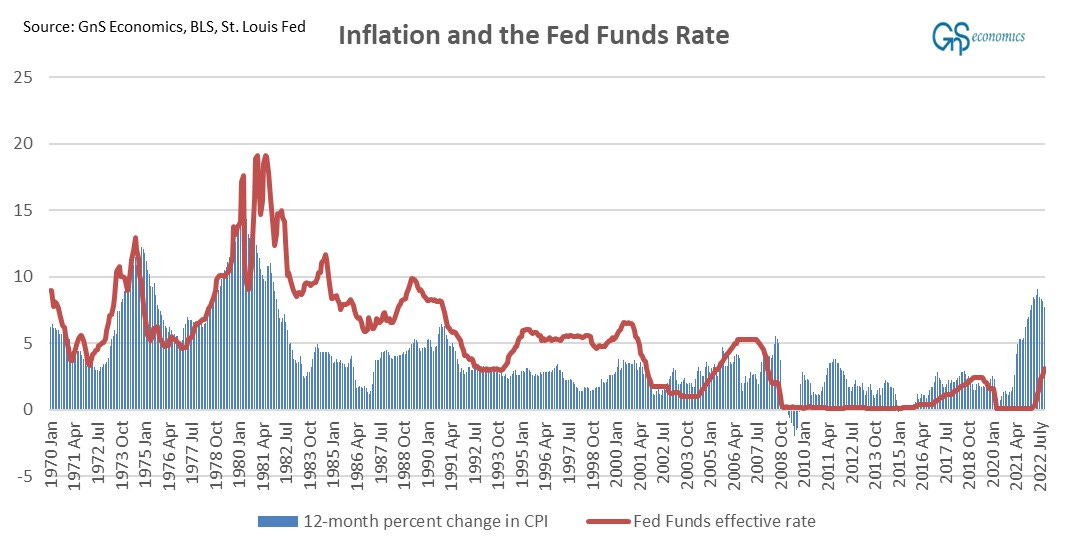

Inflation has ‘anchored’ in the U.S.

While inflation eased in the U.S. in September and October, inflation expectations have eased only marginally and have recently risen again.

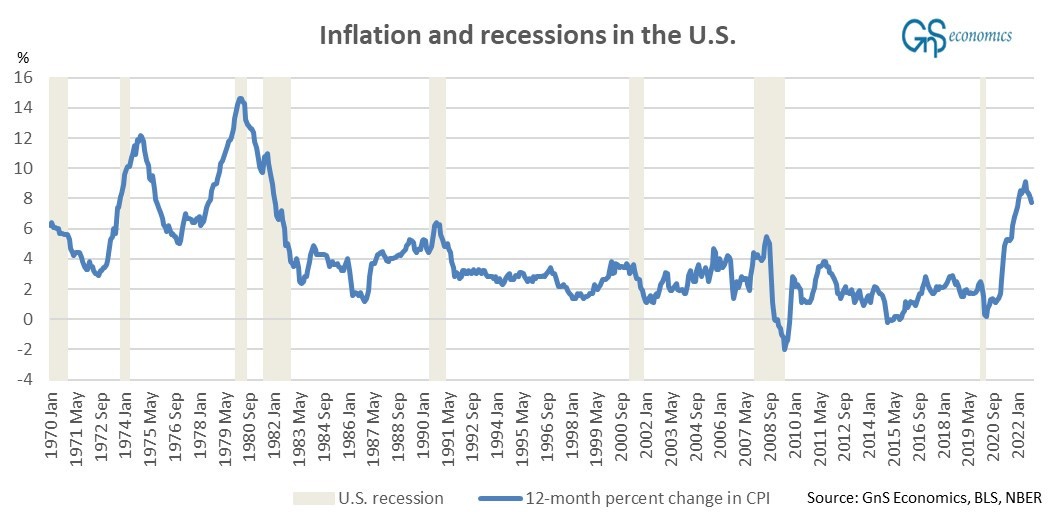

Moreover, we can see from the figure above that the U.S. is experiencing a similar kind of inflation shock than in the early 1980s, which was driven by oil embargo and wars in the Middle-East. That is, inflation is running clearly above inflation expectations. This leads to the ‘conundrum’ at hand.

It took draconian levels of interest rates, and a recession, to bring inflation down in the early 1980s. In general, interest rates have usually needed to be at or above the pace of inflation to bring it down. Currently, the Fed is nowhere near that.

Moreover, in simplified terms inflation can be described as: excess (monetary) demand over supply. That is, a persistent inflation arises, when there’s too much money chasing too small supply of goods and services.

Interest rate hikes are aimed at curbing demand by restricting borrowing of households and corporations. As banks create most of new money, through credit creation, declining bank lending will bring down the amount of money in circulation. This is why the effect of interest rate hikes becomes visible with a lag. It takes time for demand to come down or ‘cool’. Usually, bringing rapid inflation down requires a recession, i.e., heavy ‘demand destruction’.

That’s where the U.S. is heading (into a recession), so inflation will come down, eventually, but it is not so straigth-forward this time around.

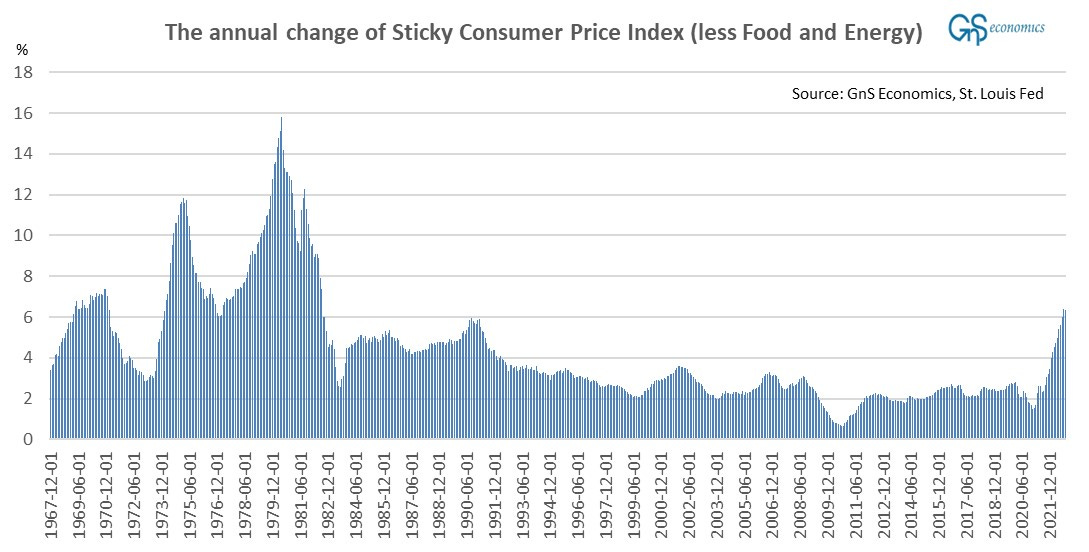

The ‘sticky inflation’ , which follows the goods and services whose prices change relatively infrequently, remains at its highest level since August 1982. This implies that inflation has become a wide-spread phenomenon. This is reflected in wages, which are, again, rising rapidly (see, e.g., this and this).

How I see this, is that inflation expectations have become “anchored” at a higher level and are likely to remain there until recession truly arrives. This means that both firms and households are expecting fast inflation to continue, which feeds into wages and price increases keeping the pace of inflation high, until labor markets ease and corporations see demand for their products falling. This (recession) may start as early as Q1 next year.

However, the ‘curve ball’ here is the situation in Europe.

European energy crisis, Phase II

The warning of the Bundesnetzagentur basically says it all. Gas flows to Germany remain heavily depressed and exports of gas from Germany have collapsed. This implies that gas prices will see heavy fluctuations across Europe, as the gas storages have started to dwindle. Price fluctuations are likely to get worse as storage levels start to fall more rapidly heading into empty.

Extraction of gas from storages began in Mid-November. While gas consumption has remained low this has been mostly driven by a decline in industry consumption. This quite straight-forwardly implies that industries have cut back production and we can expect this trend to continue in the coming months. Another word for this is: de-industrialization.

Many industries have already scaled down or ceased operations and it’s likely to turn much worse. The worst scenario, estimated by the German utilities companies, is that if Germany would experience a cold winter, similar to 2010, gas storages would be empty by the end of January. This would mean that 25% of industries would need to be shut down in February-March. Naturally, in such an event, the prices of natural gas would go through the roof. Worryingly, December is currently forecasted to be cold or even very cold across Europe.

As a small sign of relief, hydro reservoirs in the Nordpool area almost reached their long-run median two weeks ago. This drastically reduces the likelihood of rolling blackouts in Central-Europe, but does not remove their threat entirely.

It has been really hard for me to understand, why nuclear and coal power plants are still scheluded to be closed in the face of a major and prolonged energy crisis. Every estimate I have seen says the same, i.e., that the crisis will last for years. Many energy analysts argue that this will not even be the worst winter, but the 2023-24 winter would see the largest repercussion of current policies. This is, because it is uncertain whether (and from where) Europe will be able to fill their gas storages once they are emptied.

Alas, the outlook for Europe is bleak, to say the least. We are also likely to see elevated inflation pressures globally again in the coming monhts, originating from Europe.

Add the globalization ‘plot-twist’

An another thing the peak-inflation crowd seems to be missing is the ‘reshoring’ currently occurring, and likely hastening, across the globe. What this means is that companies are moving production “back home”, especially back to western countries due to supply-chain uncertainties.

This also means that the cost-benefits of outsourcing to countries with cheaper labor are being reversed implying that production costs will rise. This will keep inflation pressures high for the coming years. The whole era of low (sub-2%) inflation is likely to be at end.

Depending a bit on your preferences and indicators, this has been the either the third or the fourth period of globalization. While there were Ancient globalization periods also, we economists usually think that the first wave of globalization occurred between 1870 and 1914, the second from 1945 till 1971 and the third from 1995 till 2020 (some consider that the third wave occured in the 1980s). They were stopped by wars and other global shocks, and now we have, and are, wittnessing both. This means that we should prepare for the return of permanently higher inflation and thus higher interest rates.

In the absolute worst case, the combination of energy crisis, collapse of the financial bubble and de-industrialization could be produce a “depreflation”. That is, a collapse in economic activity (depression) combined with fast inflation driven by soaring production costs. I don’t consider this as a likely scenario, but it is theoretically possible.

Keep preparing.

Disclaimer:

The information contained herein is current as at the date of this entry. The information presented here is considered reliable, but its accuracy is not guaranteed. Changes may occur in the circumstances after the date of this entry and the information contained in this post may not hold true in the future.

No information contained in this entry should be construed as investment advice. Readers should always consult their own personal financial or investment advisor before making any investment decision, and readers using this post do so solely at their own risk.

Readers must make an independent assessment of the risks involved and of the legal, tax, business, financial or other consequences of their actions. GnS Economics nor Tuomas Malinen cannot be held i) responsible for any decision taken, act or omission; or ii) liable for damages caused by such measures.