Thoughts on Jackson Hole

Thoughts on Jackson Hole

The desperation of a central banker

Central bankers have been keeping their annual meeting in Jackson Hole in a virtual form this time around.

Yesterday, we saw the most anticipated speech, i.e. that of Jerome Powell, the Chairman of the Fed. There were also several speeches from Presidents of regional Federal Reserve Banks preceding the speech of Chair Powell.

Here are some comments regarding to these.

To taper or not to taper?

Before the speech of J. Powell, three of the most prominent “hawks” in the Federal Reserve, Dallas’s Robert Kaplan, St. Louis’s James Bullard and Kansas City’s Esther George, called for tapering, that is, the reducing of the asset purchases of the central bank. In his speech, Chair Powell was reassuring. He, for example, stated that:

The Committee remains steadfast in our often-expressed commitment to support the economy for as long as is needed to achieve a full recovery.

This was a classical ‘move’, or performance in the (current) playbook of the Federal Reserve. Give public hints, through regional Fed Presidents, that there will be a change in the Fed policy (tightening), and then walk back from that. So, essentially the policy is to ‘scare and reassure’.

However, this policy is usually used before a change in the monetary policy. The monetary policy “tool” of ‘forward guidance’, where a central bank tries to guide the perception of market participants, households and firms by hinting of a coming (planned) change in their policy, is generally applied in this manner. That is, through ‘scare and reassure (walk back)’ tactics. Thus, the announcement for tapering may come soon, even within weeks.

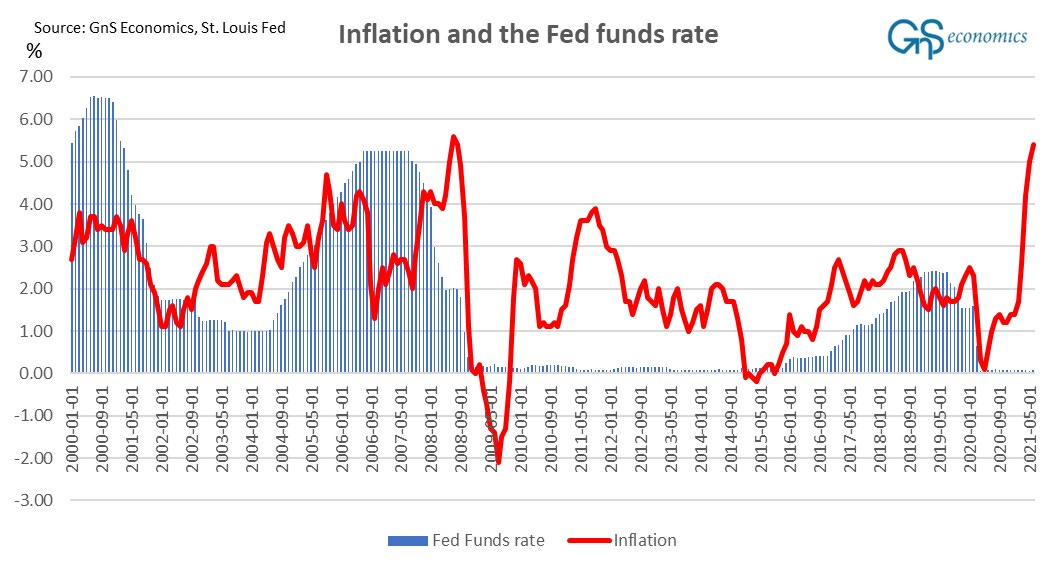

But, that’s not the main headache of the Fed now, but inflation. This figure presents their ‘pain‘ quite elegantly. The monetary policy line (Fed Funds rate) is way off the mark.

Failure in (economic) logic

In the part Chair Powell talked about inflation, we got a glimpse of the anxiety within the Fed. For example, he gave two conflicting statements on wages:

#1: The levels of job openings and quits are at record highs, and employers report that they cannot fill jobs fast enough to meet returning demand.

#2: But if wage increases were to move materially and persistently above the levels of productivity gains and inflation, businesses would likely pass those increases on to customers, a process that could become the sort of "wage–price spiral" seen at times in the past. Today we see little evidence of wage increases that might threaten excessive inflation.

So, essentially, Chair Powell first warned that recovery is so fast that employers cannot find workers to fill vacancies and then later he claimed that they don’t see wage pressures that in the data.

While their data may not show increasing wage pressures, yet, every single economist, and those with some common sense, understand that if corporations have issues filling job vacancies, when faced with (somewhat over-whelming) demand, wage increases are coming, and they may easily “spiral”.

How can Chair Powell miss this ‘non-brainer’?

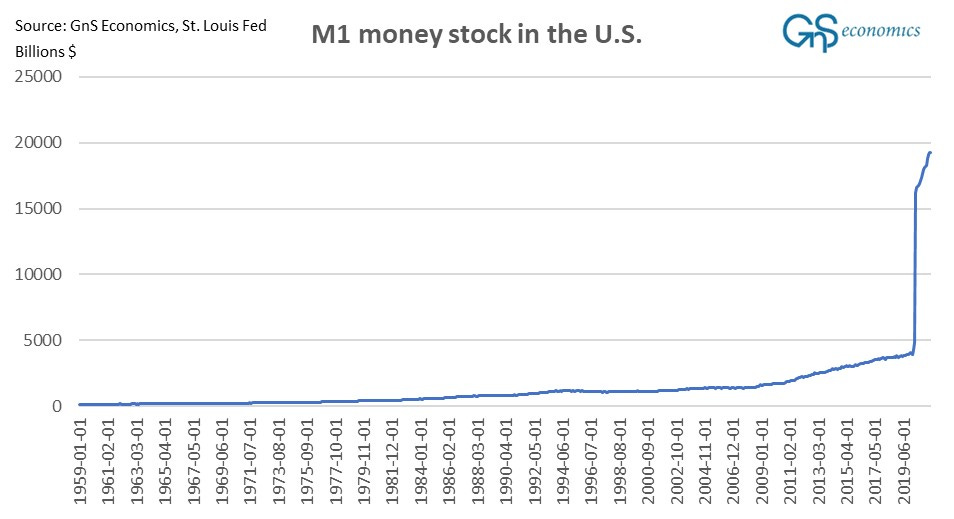

Well, for the simple reason we (GnS) and I have been warning for some time: the U.S. financial system (and most households and corporations) cannot cope with higher interest rates.

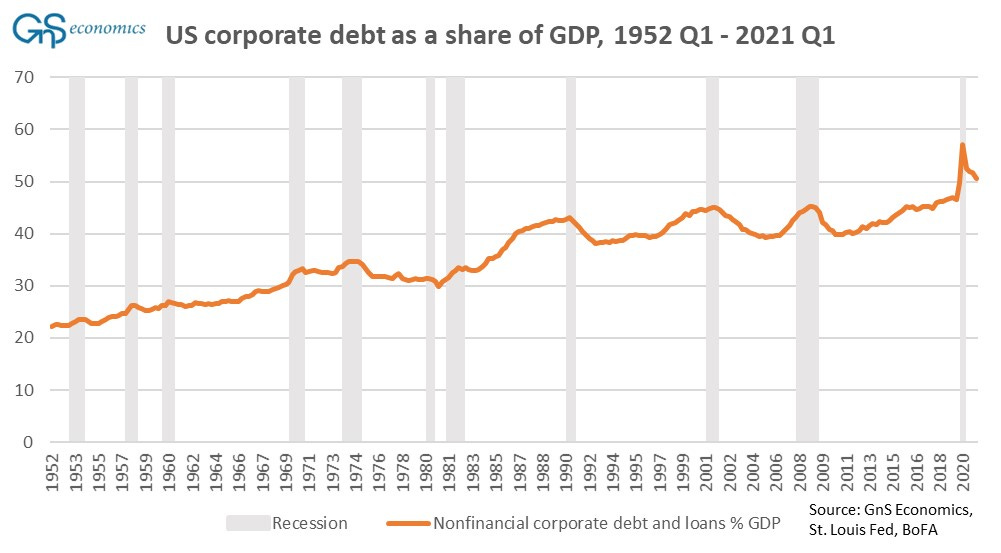

This is because the financial system is extremely-levered (for example the ‘margin debt’ reached a record of €882 billion in June), corporations are more indebted than ever and households also have very large amounts of debt.

Simplified: If the Fed raises rates aggressively, the U.S. financial system and economy are very likely to collapse.

How dangerous is a trapped central banker?

Like I’ve detailed in my previous posts, the Fed is effectively trapped. The speeches in Jackson Hole enforce this view. There was a hint of panic in the air.

Chair Powell is likely to be acutely aware of the massive financial bubble the Fed has helped to create. But, their mandate, demanding for price stability, is forcing the hand of the Fed.

This is why the Fed is doing what it’s doing, that is, talking about tightening (tapering) and walk back from it, and praying that inflation will ease. Because if it does not, the Fed will be forced to ‘face the music’, taper, raise rates, and then witness the collapse of their own creation (bubblified financial markets), and all political repercussion that will follow.

Because of the likely repercussions of tightening the monetary policy, we are also facing the truly scary possibility of runaway inflation.

Even though I don’t consider it likely, there’s the possibility that the Fed does nothing or ‘drags its feet’ too long. This would mean that it would keep pumping money into the economy through QE, which would eventually break in the monetary system leading to a hyperinflation. This would be the biggest policy mistake in the history of central banking, and I am rather certain that the Fed will not allow it to happen.

However, one never knows, how dangerous a trapped central banker is. We will soon find out.