We're doomed

The 'unholy trinity' of central bankers (Free)

Now that we have entered the GFC 2.0 (Global Financial Crisis 2.0), I will adjust my entries accordingly, as will GnS Economics. Essentially this means that we will concentrate on serving our clients and subscribers.

This is for two reasons. First, our allegiance lay with our customers. We will thus concentrate on guiding them through this crisis.

Secondly, this is the first banking crisis in the era of social media, and we also have responsibility towards the society at large. In the coming weeks, we will publish analyses on individual banks to reek out the ‘bad apples’ in the European and U.S. banking sectors. This information will not be made public, because we do not want to be the ones that create or accelerate a bank run in the current, fragile situation. That’s why the information we obtain will be made available only to our clients and subscribers of GnS Economics Newsletter.

However, in this entry, I will explain the dire situation from where our main financial authorities, central banks, found themselves. They are now confronted by the coincidental appearance of an inflation crisis, a banking crisis and a recession. Essentially, the situation is a world-first in the era of modern central banking, as they have not faced such an “unholy trinity” before.

When warnings are not heed

We have been warning on the risk of a another global banking crisis for over three years (see, e.g., this, this and this). Authorities were able to postpone it until 10 March, 2023. The failure of the Silicon Valley Bank was a symptom of a much wider problem, as I explained in my two previous posts, effectively confirmed by Treasury Secretary Yellen through her public ‘joggling’ with the idea of a wider (temporary) deposit guarantee scheme. The U.S. banking system is fragile, like we warned earlier.

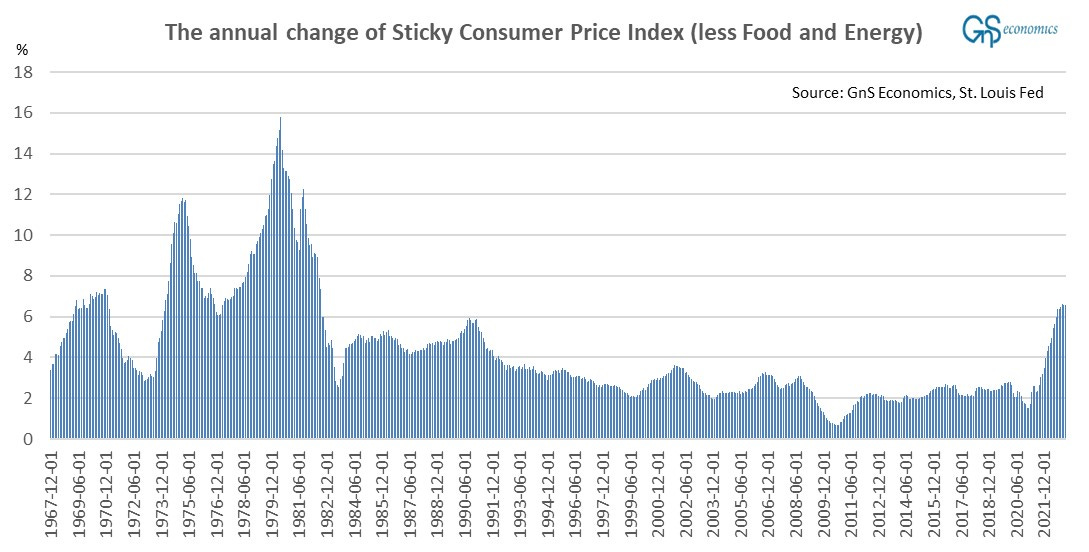

There’s an excellent piece by John Authers in Bloomberg Opinion going through the ‘unpleasantness’ of the inflation situation in the U.S. To summarize despite of the cooling of the headline figure (CPI), core inflation and especially the ‘sticky inflation’ run rampant.

On Tuesday, we learned that inflation in the U.K. had re-accelerated to 10.4% (from 10.1%). Also inflation in the euro area continues unabated with the pace of annual ‘core’ inflation reaching a record of 5.6% in February.

The simple fact is that we would most likely not be here, if central bankers would had understood in summer 2021 that the inflation shock is not “transitory” and if they had followed this by raising rates. We had warned on the approaching inflation shock in March, 2021, and we explained in July that the inflation shock is unlikely to abate, i.e. that inflation is “non-transitory”.

Basically the only reason, why the head-line inflation has come down in Europe and the U.S., has been an ‘act of God’, namely exceptionally mild-winter in Europe. Without the ‘weather Gods’ on our side, Europe would have most likely seen sky-high energy prices and rolling blackouts. We dodged them, for now, but the underlying “core” inflation has kept accelerating.

As I’ve been explaining, inflation is essentially just a mismatch between demand and supply. Rapidly growing amount of money in circulation, almost always caused by the rapid issuance of central bank credit (like QE programs), creates the potential for a ‘demand shock’ implying a rapid increase in consumption or its persistence in the wake of declining supply. If a supply shock appears in such a situation, the inelastic demand caused by vast amount of money in the hands of consumers usually leads to a spike in general price level (as supply falls, but demand does not). If the supply shock lasts longer than few months, inflation expectations start to rise. If the central bank does not react desively in this juncture, by enacting a withdrawal of money in circulation and raising rates, inflation will start to feed itself. This is what central banks failed to do during the summer, fall and winter of 2021. The Russo-Ukrainian War was just an additional supply-side shock (see, e.g., this).

Rapidly rising interest rates will push the global economy into a recession, like we have warned all through the fall. If the economy is highly indebted (levered), like it is now, rising interest rates will threaten the solvency of financial institution and eventually the government. The first signs of this emerged in September and October past year, when British pension funds were at the brink of market-crashing fire sales and the problems of Credit Suisse (re-)emerged. They were hidden with a temporary burst of central bank liquidity, but the tightening cycle continued and then, in around mid-March, the U.S. and European banking system faced their day of reckoning.

Central banker’s trap

The original purpose of central banks were to act a emergency liquidity backstop for ailing financial institutions. The idea was that they would act as “lenders of last resort” to otherwise solvent financial institution facing temporary liquidity issues. Then their role evolved to handling the foreign exchange market and on providing financial services to the rulers. Soon after this it was discovered that lending vast amounts of money from the central bank to maintain government consumption was an extremely bad idea leading to runaway inflation (hyperinflation).

The seed of the ‘unholy trinity’ of central banking was sown, when the Federal Reserve was created in 1914. Against its original aim, the Fed soon started manipulate the economy by manipulating the interest rates of central bank reserves and through buying of government securities (Treasury notes and bills). In the 1980’s, the Fed became a financial market backstopper, when its Chairman Alan Greenspan created the ‘Greenspan put’ to help financial markets to recover after a rout.

In recent years, the Federal Reserve has “evolved” into a lender-or-last-resort of, basically, all financial institutions, capital markets, and lastly depositors through the Bank Term Funding Program (see my previous entry). The Federal Reserve has assumed a massive a role, a socialization of the U.S. economy, which was the main fear of opponents of its creation in the U.S. Congress.

Now, with all its meddling, Federal Reserve has managed to paint itself into a corner. They simply cannot save the financial markets, the economy and the banking sector at the same time, because they have opposite needs.

The financial markets need stable rates and QE to sustain market pricing. The economy needs higher rates to bring down inflation expectations that are in risk of becoming anchored yet to an even higher level. The banking sector needs deeply lower rates to ease collateral issues (price of government bonds; we detail this next week), but also deposit guarantees through additional liquidity provisions to halt the run on their liabilities (deposits).

This simply cannot be done. Demands of economic sectors are pulling the Fed into different directions. Years of meddling and assuming role way past its mandate has led the Fed to a ‘central banker’s trap’, and the ECB is not far behind. The only silver lining is that the credit depression brought upon by recession and banking crisis will eventually turn inflation into a deflation, but the road there will be very painful.

Only bad or utterly dismal options exist. We are doomed.

Disclaimer:

The information contained herein is current as at the date of this entry. The information presented here is considered reliable, but its accuracy is not guaranteed. Changes may occur in the circumstances after the date of this entry and the information contained in this post may not hold true in the future.

No information contained in this entry should be construed as investment advice. Readers should always consult their own personal financial or investment advisor before making any investment decision, and readers using this post do so solely at their own risk.

Readers must make an independent assessment of the risks involved and of the legal, tax, business, financial or other consequences of their actions. GnS Economics nor Tuomas Malinen cannot be held i) responsible for any decision taken, act or omission; or ii) liable for damages caused by such measures.