Exit the Dragon

The collapse of China (Free)

Issues discussed:

China has carried the world economy since 2009.

China’s economic model is effectively broken (“maxed out”), which has some dire implications for the world economy.

The global ‘Minsky moment’, I warned on in August, is likely to be upon us (or we are very close).

On 7 February, GnS Economics issued a warning on the state of the U.S. banking sector, which I urge you to check out.

The economic doom-and-gloom touted by me, and by GnS Economics, has but one origin: China. I think I’ve told this story before, but our dark view arose in the wilderness of western Lapland. Me and my ex-wife had a habit of spending the New Year in a small resort village near Pallastunturi. We hiked in the fell, went skiing, hunted for Northern Lights and just enjoyed the calmness and beauty of the polar nights.

In late 2016, we were there again, and my ex-wife was reading Thinking Fast and Slow by Daniel Kahneman. The book deals with human decision making and especially rational and non-rational motivations, or triggers, associated with human decisions. One of the subtopics of the book is errors in forecasting. We started talking about our forecasts and I told her that “I think that something is seriously off with the world economy, and our forecasts”. This was because the world economy had slowed notably in 2015, only to shoot up from the brink of a recession a year after without any clear explanation. She replied by asking am I sure that I am not simply following my previous (erroneous) thinking, or “Inside view”, as described by Dr. Kahneman. This got me thinking, and when we got home, I trashed all the data and models we had been using, and started over.

Three months later, we published our first “doom-and-gloom” quarterly report, Bellwethers of a Fall, where we issued our first ever warning of a global crash. I had discovered that the world economy had never truly recovered from the Great Financial Crisis of 2007-2008. Everything in the financial markets had just become supported by the central banks, as depicted in the figure below (straight from the report). However, while it was apparent that central banks saved the financial markets, it left me wondering who had resuscitated the world economy?

Enter the dragon

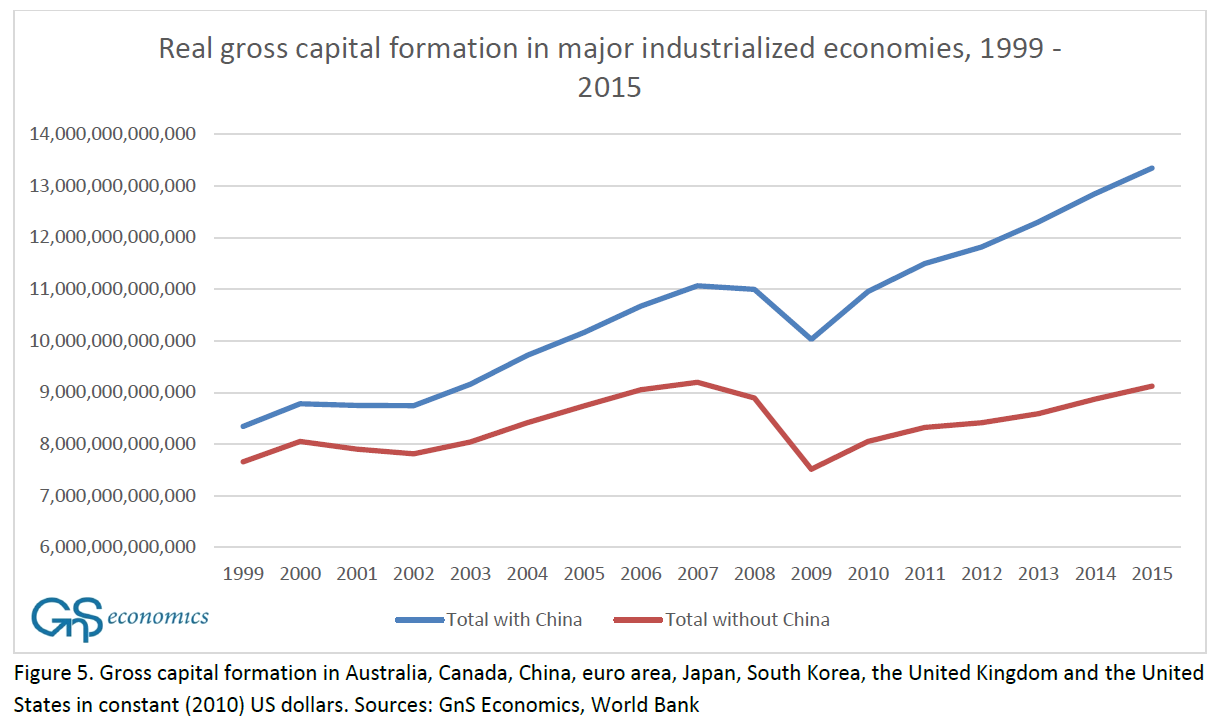

The answer presented itself during the following summer. After another round of excessive data-mining, I learned that China had rescued the world economy in 2009 with massive debt stimulus. We published my findings in a report entitled: The World Economy on the Brink. Most notably, China had been responsible for almost all of the creation of private debt in the world and most of capital investments since 2009 (figures are straight from the report).

Still, one thing bugged me. As there was no sudden spike visible in the debt statistics of China, where had the money for the stimulus and rapid acceleration of economic growth come from?

I kept on digging and found the answer in early 2018. It was published in March 2018, as a part of our special report on quantitative easing/tightening (asset purchase/roll-off) programs of central banks. The next figure depicts the reason why the world economy recovered so rapidly in 2016 “without a trace”.

In 2015/2016, China had run a gargantuan stimulus program financed through the shadow banking sector. “Shadow banking sector” is just a fancy name for financial corporations providing lending to corporations and local governments outside the traditional, regulated banking sector. In just one year (2016), the balance sheets of shadow banks grew from around $12 trillion to over $38 trillion. This means that in just one year, China’s banking sector grew into a bloated behemoth. The unsustainability of the credit binge became painfully obvious, when we compared the size of the banking sector of China to that of the U.S. right before it collapsed in the Great Financial Crisis.

The dominating role China has held on the world economy since 2009 (see also this) makes her current economic woes very worrying. As we warned in October 2017:

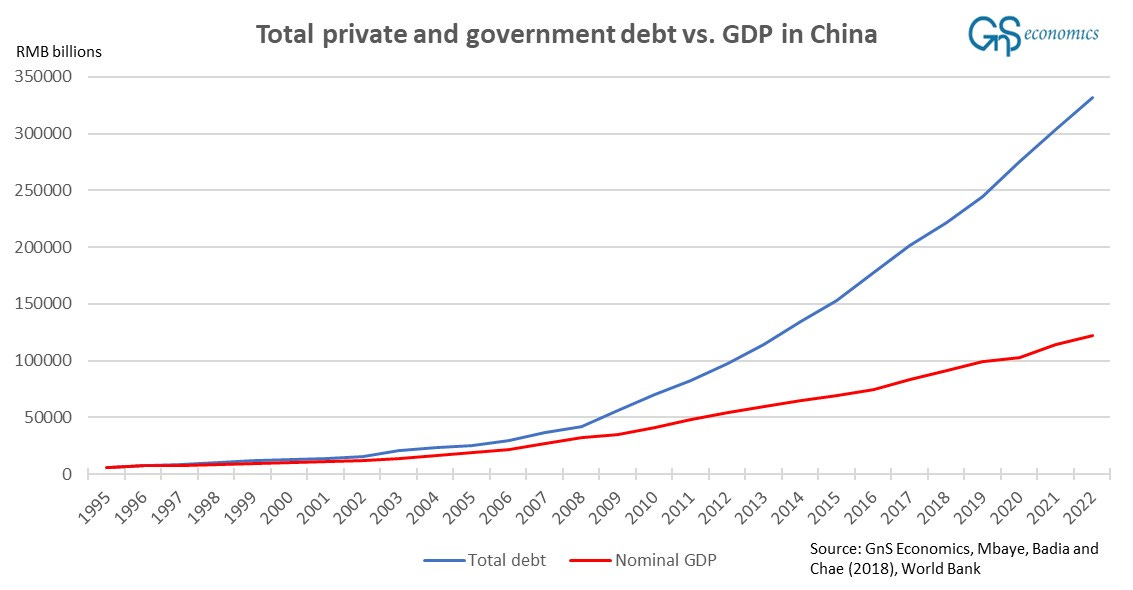

If the asset value destruction starts, and the “jump” happens in China, it will be followed by debt destruction or deflation. Because China has been responsible for over 95 % of global private debt creation since 2008 (see the figure below), global private debt will start to contract (unless other large economies and corporations commence a massive investment spree, which is unlikely). This China-induced global debt deflation will mean a global asset deflation, and thus a global ‘Minsky moment’. So, if China faces a Minsky moment, the world, with high probability, will face it also.

Everything that is now manifesting in China is related 1) to her major debt stimulus which ran from 2009 on, and 2) to the gargantuan credit binge enacted through the shadow banking sector in 2016. (More on the Minsky moment below.)

Let’s now take a closer look at how bad the situation in China currently is.

Exit the dragon

On Monday (5 February), the Chinese stock market fell more than 8%. and it was down 30% on the start of the year. During the day, trading on almost 30% of Chinese stocks were halted due to limit down. There was a rather clear bailout attempt, most likely by the “National Team” (essentially China’s plunge protection team) after midday, but this failed to halt the selling.

However, the powers of Beijing to control the financial sector are vast. On Monday (5 February), Kobeissi Letter and Bloomberg reported that Beijing has issued several restrictions to trading. These included:

Limiting investors' ability to short Hong Kong stocks, while some investor operating in mainland China were told not to reduce their positions.

Some investors were told that they are not allowed to sell their positions.

Some quant funds were completely banned from placing sell orders.

Other quants funds banned from cutting leveraged positions.

At first, they failed to halt the selling, but on Tuesday the 6th we saw frantic buying mostly due to a severely over-sold market and because of news breaking that Beijing was considering another set of measures to calm the turmoil in the financial markets. The vast powers Beijing holds have made it possible for it to halt severe selling periods and control the de-leveraging of the economy and the financial sector in the past, but I suspect that this has now changed.

I consider that the selling has been driven by a massive de-leveraging of the shadow banking sector. Like GnS Economics noted in the January Outlook, this became visible in the failure of shadow banking conglomerate Zhongzhi Enterprise Group. The forced liquidation, by a Hong Kong court, of the troubled property developer Evergrande was another major “warning shot” pushing investors, and households, to franticly de-leverage (selling).

Moreover, like GnS Economics warned in July, the Chinese economy seems to have reached ‘debt saturation’, which implies that households and corporations will not, or cannot, absorb any more debt. Because China is an extremely indebted economy, this implies that a violent de-leveraging, a Minsky moment,1 has arrived. This is visible in the crashing real estate and asset markets, as well as severe banking troubles especially in the “shadowy” side, which all indicate that a Minsky moment in China is upon us.

The question is, can Beijing stop it, and what happens if it cannot? I suspect it cannot, although it may be able to postpone and control the de-leveraging for some time still.

Maxed out

The problem faced by Beijing is two-fold:

Economic growth requires leveraging (debt issuance), but

Debt saturation has been reached in almost all levels of the economy.

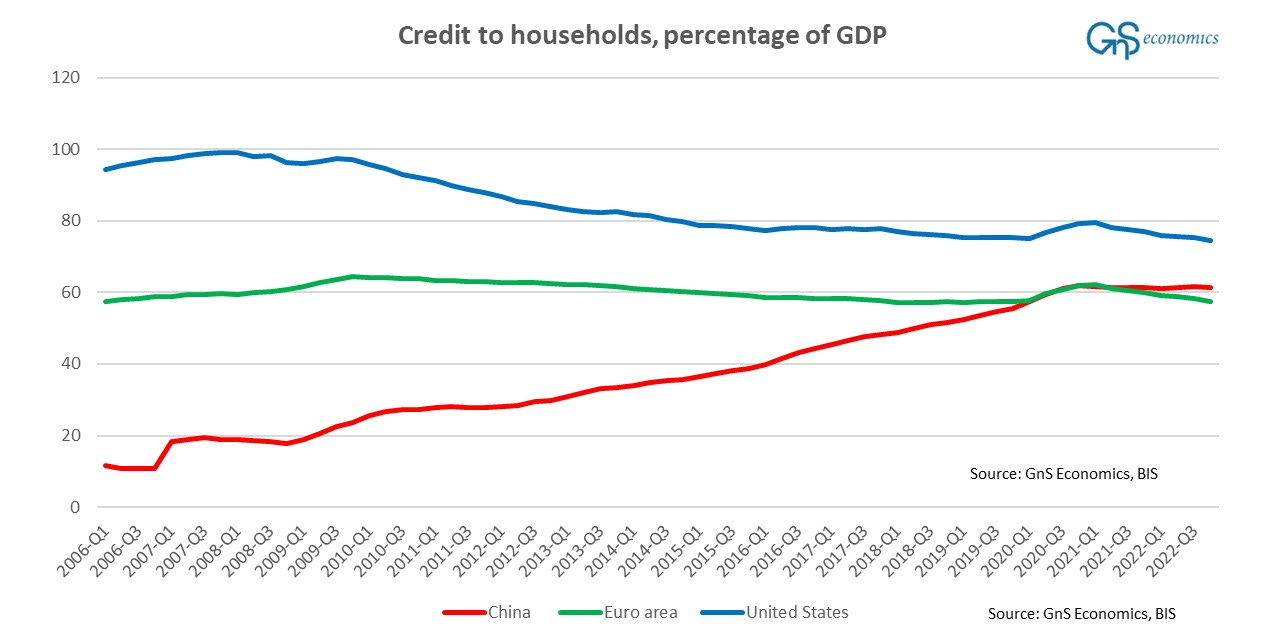

The most telling picture on the extremity of the debt situation of China is this.

Alas, basically every entity in the Chinese economy is heavily indebted. Non-financial corporate debt was over 133% of GDP at the end of 2022 (vs. around 80% in the U.S). At the end of past year, household debt (credit) was at similarly horrific levels, considering that China is still a developing economy.

And, the local government sector, which has been the main borrower and thus the main source of economic growth, since 2016, is likely to be deep in de-leveraging. The Rhodium Group has conducted excellent research on it, which I urge you to check out. They found, for example, that at the end of 2022 only around one-fifth of the local government financing vehicles (LGFVs), which were the counterpart of local governments to the lending from the shadow banking sector (or a part of it), could cover their short-term debt obligations, including interest payments. This implies that thousands of LGFVs are underwater with their debts clearly exceeding the value of assets (real estate) local governments purchased (built) with that money. This is the main culprit behind the collapse of the real estate sector, as local governments were the main financiers of real estate projects (with the money they borrowed through the LGFVs from the shadow banks). This is the Minsky moment.

Moreover, there really is no easy solution to this. The only entity with some leeway considering debt, is the central government (Beijing). However, with its debt fast approaching 80% of GDP, that leeway is getting narrower by the hour.

I am suspecting that there is very little that Beijing, or anyone else for matter, can do to save China’s economy. Reports on the ground tell a heart-breaking story of firm closures and empty malls (I sometimes watch, e.g., China Observer, but note that you need some '“filters” with their content). Beijing may be able to buy some time, but as the Minsky moment has, most likely, arrived, it cannot be undone. This means that violent de-leveraging of the Chinese economy will continue, even though we may see short (1-3 month long) pauses in it.

We are in deep trouble.

Disclaimer:

The information contained herein is current as at the date of this entry. The information presented here is considered reliable, but its accuracy is not guaranteed. Changes may occur in the circumstances after the date of this entry and the information contained in this post may not hold true in the future.

No information contained in this entry should be construed as investment advice. GnS Economics nor Tuomas Malinen cannot be held responsible for errors or omissions in the data presented. Readers should always consult their own personal financial or investment advisor before making any investment decision, and readers using this post do so solely at their own risk.

Readers must make an independent assessment of the risks involved and of the legal, tax, business, financial or other consequences of their actions. GnS Economics nor Tuomas Malinen cannot be held i) responsible for any decision taken, act or omission; or ii) liable for damages caused by such measures.

In a Minsky moment, asset valuations suddenly start to lose value en masse. Technically, it is a sudden jump of the distribution of the asset yields into the negative, driven by frantic liquidation of stocks, debt and real estate by households and corporations.

I agree on most things you write in other articles, but not on the issue of China . Probably you also became victim of mass overwhelming anti China hysteria/propaganda.

Which doesn't mean that I believe situation in China is great.

I think that you severely underestimate the power of government/rulers in the command economy. There are many more things that could be enacted or outruled, that haven't been started yet, it is just a question of their willingness and true goals...

I wasn't aware of the bellow debt number and I see it as completely oposite - that the central government (Beijing) has a significant leeway increasing debt and stimulating growth if they decide so... Especially when real estate is not attractive as investment to many Chinese anymore, which means that many bonds could be sold domestically. I havebto point out also, that the PBOC hasn't been buying bonds till now in huge contrast to the Western CBs. The ruler recently said that that should be enacted. So there is a gargantous leeway available from that source as well.

Moreover, there really is no easy solution to this. The only entity with some leeway considering debt, is the central government (Beijing). However, with its debt fast approaching 80% of GDP, that leeway is getting narrower by the hour.