From an inflation shock to an inflation crisis?

A path paved with good intentions

In March, we warned on the approaching “inflation shock”. We wrote:

In research published in November, the International Monetary Fund, or IMF, found that inflation was noticeably faster than the rate calculated by standard inflation measures in all regions. The reason behind this has been the change in consumption patterns.

There have been reports of serious bottlenecks in the transport of vast quantities of commodities, which has lifted prices. So, inflation has been running higher than shown in the official figures, but the real problems are likely to emerge when economies re-open and conditions move towards a “new normal”, which is now occurring in the U.S. Airlines, hotels, restaurants, etc., now have diminished capacity, which means that they may be unable to meet suddenly increased demand. And the prices for services may see a sudden uptick which, combined with the already fast-increasing price of commodities, could lead to an abrupt and unexpected rise in the inflation rate when economies are operating more fully.

So, the building blocks for the ‘inflation shock’ were plainly visible under the surface of standard inflation measures.

How come so many analysts were unable to see this, is an interesting question. It’s likely that they were looking at standard measures of inflation, which were benignly low creating a false sense of security.

But, there’s likely more to come.

Building blocks of a rapid inflation

Inflation is a monetary phenomenon in a sense that, when there’s too much money in circulation, or “chasing” products, the prices of commodities tend to increase. Remember that money is essentially just the measure of prices of commodities and assets. When there’s a lot of money, prices rise as a result.

Like I explained in my previous post, this is effectively what QE -programs have done in the financial markets. They have pushed yields of government and corporate debt down, artificially. Moreover, they have created massive amounts of artificial, that is, central bank created liquidity (deposits). Recently, banks have become unable to handle this continuing increase in the cash forced upon them by the QE:s, which I detailed in this post.

What was a reasonably controlled increase in the monetary base of the U.S. economy turned to something very different, when the Fed decided to bailout the U.S. economy after the ‘corona shock’ (lockdowns) during the Spring of 2020 (see, e.g., this WSJ article for some details of the actions taken by the Fed).

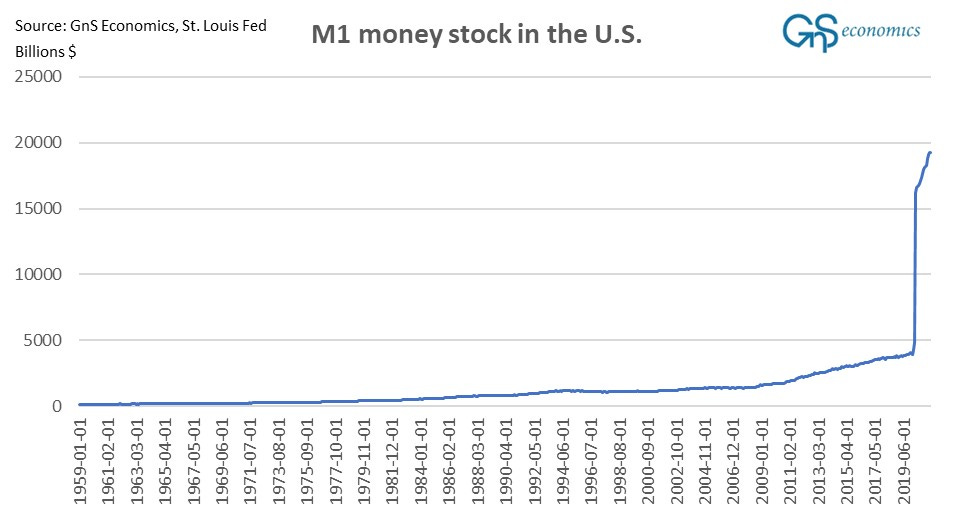

This monetary meddling pushed the M1 monetary aggregate, which consists of demand deposits and checking accounts into an insane vertical ‘pivot’. Through this, the Federal Reserve has subjected the economy to the possibility of a ravaging inflation.

But, why it took so long for the inflation to arrive?

Creating a ‘time bomb’

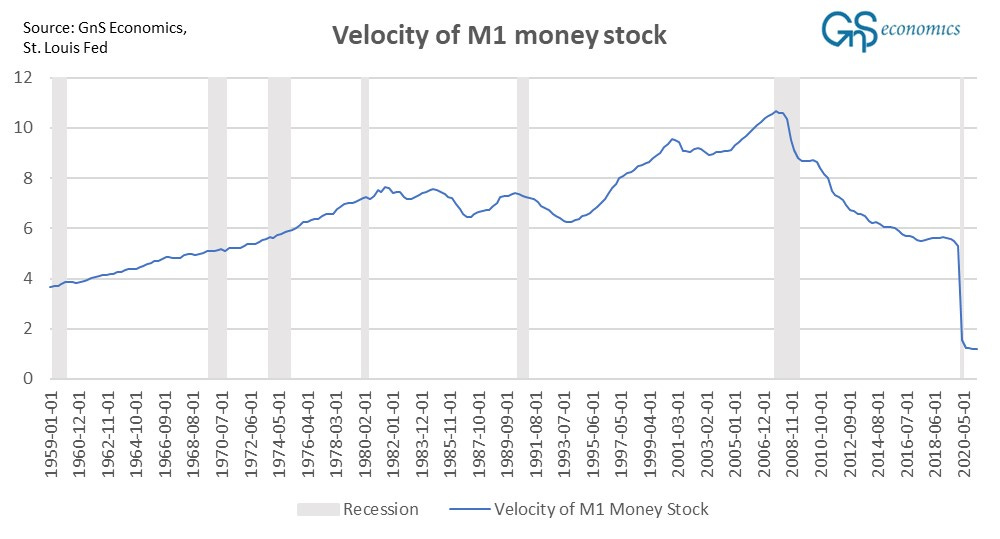

At the same time, when the money in the deposit and checking accounts exploded, the velocity of money, calculated as the ratio of gross domestic product and the M1 money stock, collapsed driven by the economic activity (and massive increase in the M1 stock).

This is another part of the dangerous “artificiality” of the monetary resuscitation of the economy through QE. It corrupts the normal relation between money and economic activity.

Now just imagine what would happen if the velocity of money would suddenly increase even to a ratio of four? Massive amounts of money would be hunting a limited supply of products. Prices of commodities would simply explode.

Supply-chain issues

There’s an excellent blog going through the recent developments in the world of global freight. Essentially the problem is two-fold: port closures linked to corona infections and congestion of the main ports in China and the U.S.

These will increase price pressures of commodities by increasing the prices of freight. Inceases in freight prices after the corona outbreak have been notable. For example, prices in the Freightos global container freight index have exploded nine-fold since February 2020, and now it’s on the rise again.

Like we saw last winter, localized coronavirus infections can shutdown factories and warehouses leading to unexpected disruptions in commodities and key components. Thus, as the waves of the coronavirus are likely to continue in the fall, we can expect more supply-chain disruptions keeping pressure on prices.

Towards an inflation crisis

We are now faced with several factors increasing the likelihood of hastening and persistent inflation.

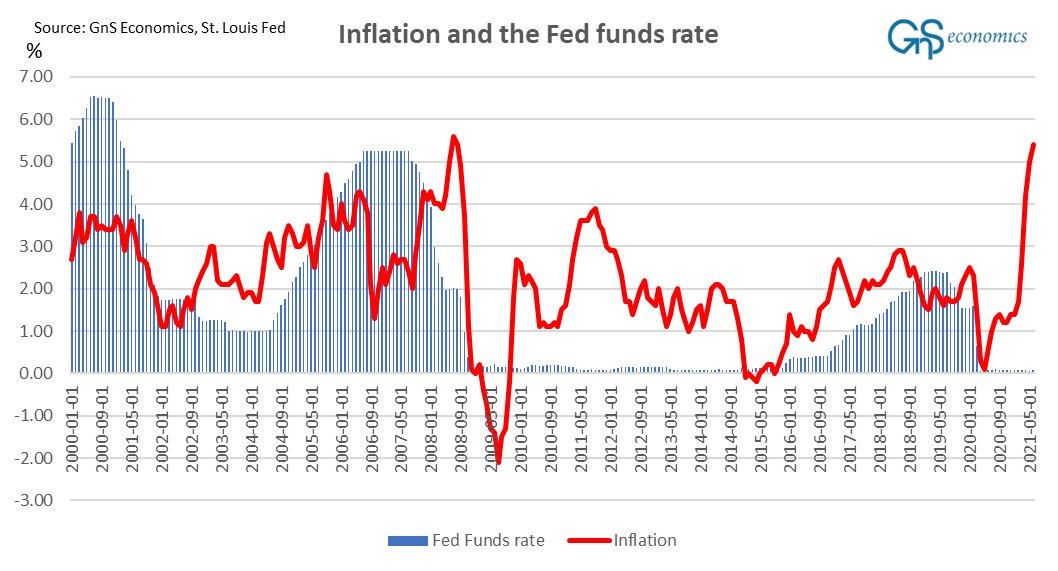

Inflation in the U.S. “steadied” at 5.4% in July, which was the same figure as in June. The “core” index (excluding food and energy) rose by 4.3%, which means that inflation has accelerated in a broad range of commodities. This implies that inflation is becoming more persistent.

Port congestion and closures as well as other issues with freight (like the ‘trucker shortage’) will keep pressure on transportation and freight prices.

Central banks, especially the Fed, has pushed massive amounts of money into the economy through QE:s. After the wave caused by the Delta-variant peaks, this money may start to “exchange hands” faster which, combined with the freight issues, would lead to a situation, where large amounts of money would be chasing fewer products. This would give rise to a ever-faster, possibly exploding inflation (more on this later).

Alas, we may be approaching an inflation crisis. And then we may truly start to wonder, what will the central banks do? Essentially, they would have no other options than to rise rates, as for example the legal mandate of the Fed demands that the central banks keeps inflation in check.

And, when rates rise, what happens to the extremely-levered asset and credit markets? Nothing good, is my take.