The inflation conundrum

When all you got is a hammer...

Issues contributed:

The monetary shock, the main driver of inflation in the U.S., has a long way to go.

Inflation picture in the Eurozone remains very difficult.

The policy mistakes that led inflation to spike are not easy to revert.

Inflation has slowed notably during the past few months. In the U.S. the (annualized) Consumer Price Index (CPI) rose by 4.9% in April and in the Eurozone the Harmonized Index of Consumer Prices (HICP) rose by 7.0%. In March, CPI rose by 5% and HICP by 6.9%. The ‘core’ sticky price CPI of the U.S., tracking goods whose prices change relatively infrequently (less food and energy), rose by 6.3% in April, a marginal easing from the peak-growth of over 6.6% in December. The core inflation (excluding energy, food, alcohol & tobacco) grew by 5.6% in April in the Eurozone, which was barely below the peak-growth of 5.7% reached in March.

The easy gains in the fight against inflation have essentially been depleted, and now the true ‘battle’ begins. The very rapid growth of core inflation implies that inflation expectation have become anchored (meaning that consumers and corporations are expecting inflation to continue rapid leading to increased wage and price pressures), which implies that rough measures are required to bring it down. We actually warned on this already in June 2021, when we argued that inflation will not be “transitory”:

If wage pressures increase, inflation expectations increase and this will translate into higher wages and prices set by corporations fuelling faster inflation, long-term. Presently there are also serious bottlenecks in supply, such as hiring difficulties, creating inflation pressures. When the prices of ‘necessities’ start to rise in the U.S., the largest economy in the world, they tend to also rise elsewhere—albeit with a lag.

I also warned in my newsletter in mid-December 2021 that if inflation is allowed to accelerate any further, heavy measures will be needed to bring it down.

What many analysts seem to fail to understand is that we are now exactly at the point, where premature rate cuts would be likely to lead to re-acceleration of inflation. The possibly even more worrying issue is that the drivers of inflation somewhat differ between the U.S. and the Eurozone, but both central banks are issuing the same ‘remedy’.

Let’s analyze the situation in the U.S. vs. the Eurozone a bit further.

The monetary shock in the U.S.

I have detailed the effects of the massive increase of the balance sheet of central banks to the amount of money in circulation in several past entries (see, e.g., this, this and this). But, how has this affected inflation?

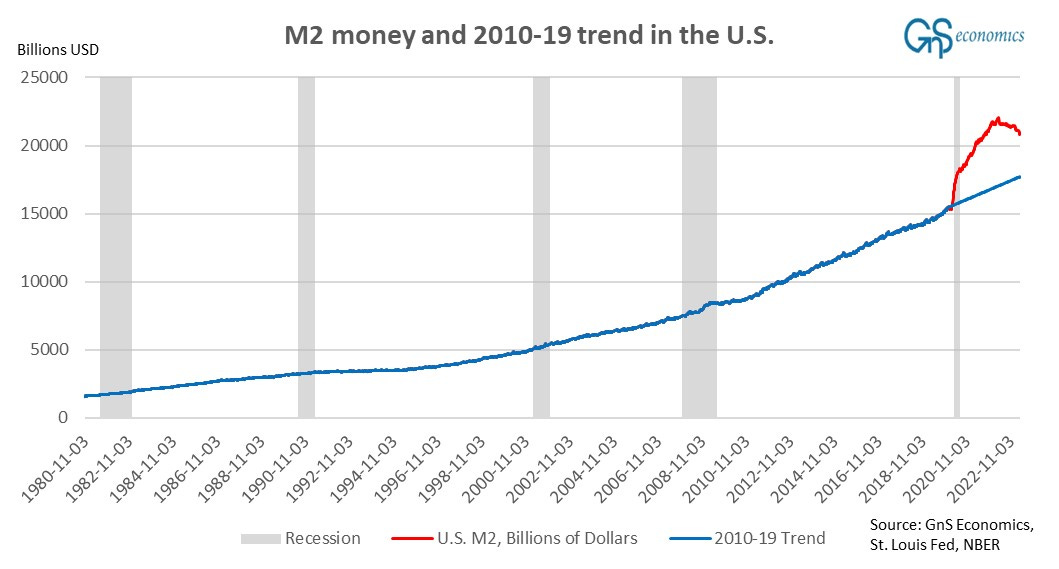

In this figure, I have calculated a trend of M2 money in the U.S. from the beginning of 2010 till the end of 2019,1 and plotted it against the actual level of M2 from January 2010 till early April 2023. The figure, quite undisputable, depicts the relentless growth in the supply of money in excess of its long-term trend from March 2020 till peak in mid-April 2022.

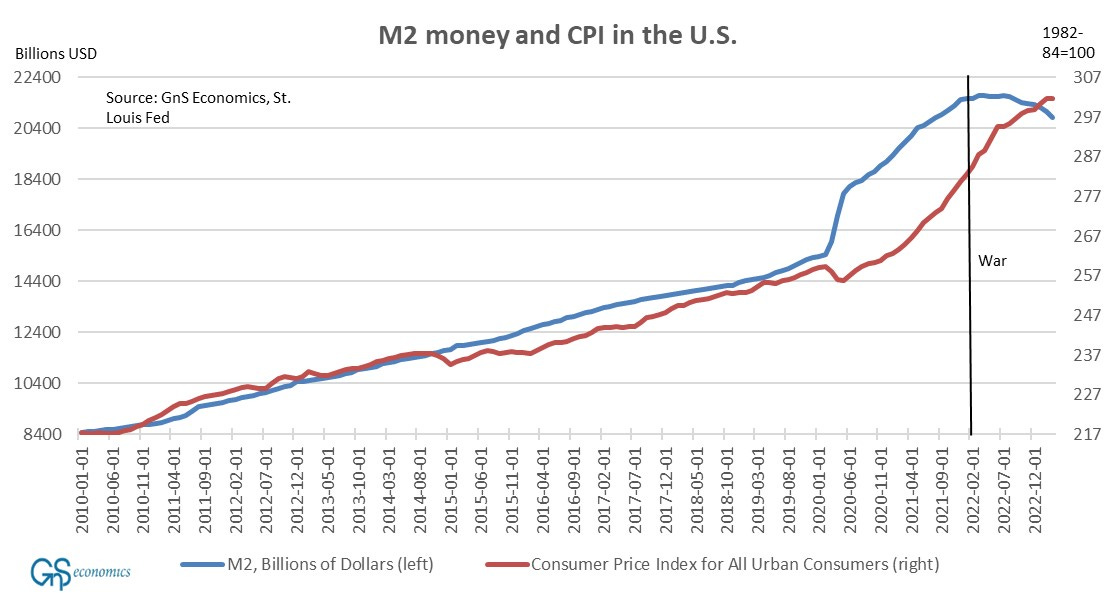

At the beginning of April, 2023, the amount of M2 was still some $3+ trillion over its 2010-2019 trend. The next figure depicts the level of CPI and M2 money in the U.S.

I think this figure tells it all. The massive increase in the amount of money in circulation, caused by the actions of the Fed and the stimulus checks of the U.S. government, pushed inflation into a rapid acceleration. The Russo-Ukrainian war just hastened the acceleration a bit. This follows the general rule of inflation that, when there’s excess money chasing goods and services, their prices tend to rise.

Now that the the amount of M2 money is declining very rapidly, it has started to bring the rate of inflation down. There’s, however, quite a bit further to go before the amount of M2 money reaches its long-term trend. Until this occurs, inflation pressures are likely to remain elevated. We got a reminder of this just this week with the University of Michigan long-term inflation expectation of consumers shooting up (Source: The Daily Shot). This is not what the Fed is looking for.

From the above we can conclude that it will take some time, before inflation rate slows to the 2% target of the Federal Reserve, and that it will most likely require the Fed to keep interest rates high for an extended period of time.

The ‘War-zone’

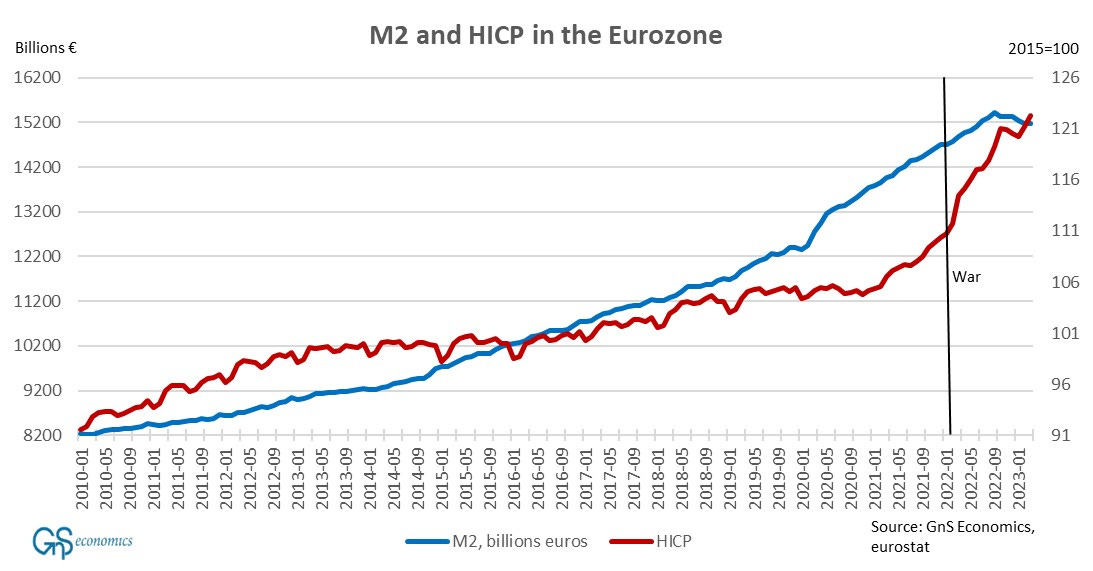

While the effects of war to inflation in the U.S. have been muted, they have had a notable effect on the path of inflation in the Eurozone. This figure shows the amount of M2 and the level of HICP in the Eurozone from January 2010 till March 2023.

It’s notable that M2 has grown rather moderately in the Eurozone, since the Corona shock of 2020, compared to the U.S. The ECB never took the drastic actions the Fed did (essentially to stop the collapse of the financial markets of the U.S.). This, the war-shock and sanctions against Russia notably hastened the pace of inflation in the Eurozone, while inflation was in an accelerating trend already before them.

The pace of inflation is also very heterogenous across the currency union. For example, Latvia saw the biggest (annualized) increase in the HICP in April (15.0%) while Luxembourg saw the smallest (2.7%). Inflation expectations also accelerated in April. This was actually the original fear of many economists, when the euro area was set up. That is, that inflation rates would diverge heavily across the EMU leading the ECB to lose control of monetary policy. We can safely conclude that we have now reached that point.

Because the war has been so crucial as a driver of inflation in the euro area, accomplishing peace, or even a ceasefire, in Ukraine would probably help much more than the rate hikes of the ECB. Peace, unfortunately, currently looks rather unlikely.

Policy mistakes in two layers

We can thus conclude that the current inflation crisis was caused by two major policy failures:

Stimulus checks and bailout of the financial markets by the Fed creating a massive increase in the amount of money in circulation, and

Failure to prevent the onset of war between Russia and Ukraine.

Moreover, because the Fed will, most likely, not want to make another mistake of easing too early (like in the 1970’s), the FOMC (Federal Open Market Committee) may push rates higher and keep them there longer than what would be needed. Alas, there’s a risk for another policy failure, namely an over-shoot, because credit crunch is likely to accelerate the decline of the M2. This implies that the Fed may, partly unwillingly, push U.S. into a deep recession, which can cause another Great Depression due to the weak state of U.S. regional banking sector (more on this later). The May Deprcon Outlook will be a special issue concentrating on the credit crunch.

The failure of central banking in the U.S. and in the Eurozone should now be clear to everyone. The massive increase in the supply of money, combined with the utterly failed “transitory inflation” narrative, makes the Fed the main culprit behind the inflation crisis in the U.S. They have hastily tried to fix their mistake by a record-breaking hiking cycle and are in a risk of overdoing it in the future.

The ECB, on the other hand, let inflation to accelerate only to be fueled further by the war. Now they have only monetary policy to respond. The ‘Green agenda’ also makes the Eurozone vulnerable to another energy shock during the winter.

Inflation shock was caused by a combination of policy failures, but it seems that only one solution is offered to solving it. If the only tool you have is a hammer, you tend to see every problem as a nail.2

Disclaimer:

The information contained herein is current as at the date of this entry. The information presented here is considered reliable, but its accuracy is not guaranteed. Changes may occur in the circumstances after the date of this entry and the information contained in this post may not hold true in the future.

No information contained in this entry should be construed as investment advice. GnS Economics nor Tuomas Malinen cannot be held responsible for errors or omissions in the data presented. Readers should always consult their own personal financial or investment advisor before making any investment decision, and readers using this post do so solely at their own risk.

Readers must make an independent assessment of the risks involved and of the legal, tax, business, financial or other consequences of their actions. GnS Economics nor Tuomas Malinen cannot be held i) responsible for any decision taken, act or omission; or ii) liable for damages caused by such measures.

The trend was calculated using an ordinary least squares (OLS) -method.

A quote by Abraham Maslow.

So the only way to slay inflation is to keep rates high but it is leading to a depression that they think they hope to control. Who would want to lead a central bank?